Your summer investing checklist

Alex Janiaud

15 min

The new tax year is already ticking. Here's a practical checklist that could help you reduce your tax bill, grow your pension and make the most of your allowances this summer.

At a glance

- Check your goals. It’s worth regularly reviewing what you’re trying to achieve with your money

- Review your cash buffer. Does it still amount to three to six months' essential expenses?

- Check your pension contributions: increasing them might lower the amount of tax you pay and could unlock childcare benefits

- Now could be a good time to think about how to use your annual Capital Gains Tax (CGT) allowance tactically – possibly in tandem with a partner – over several years.

1. Have you thought about your financial goals recently?

While not everyone thinks about setting objectives when it comes to their finances, we think having a few goals can help to organise how to allocate your money. These goals will depend on a few factors, such as your life stage and how much you can afford to invest during the tax year.

These goals should ideally be measurable. For example, some people may think about investing tax-efficiently as a goal, but this is more of a method that investors can use to pursue an objective, such as buying their first home.

Use ‘time buckets’

One issue that people face when deciding on financial objectives is juggling goals across different time horizons, such as simultaneously investing towards a house deposit and retirement.

Using ‘time buckets’ can be helpful when setting multiple goals. Break down what you’d like to achieve in the short-term (three to five years), short-to-medium-term (six to eight years), medium-to-long-term (nine to 11 years), and long-term (beyond 12 years). Then allocate goals to each of these buckets.

In practice, this could look like the following:

Short-term: save towards a month-long trip you’ve scheduled for four years' time

Medium-term: invest towards buying your first home with the aim of putting down a deposit in six years

Long-term: starting your own business in 10 years.

You can set up multiple investing pots for different goals – or time buckets – with J.P. Morgan Personal investing.

Have your circumstances changed?

It’s a good idea to periodically review these goals. Changes to your salary, sudden windfalls and other life events can alter the time it might take to achieve your financial objectives. Market volatility can also make it more challenging to invest towards short-term goals. Government announcements and changes to regulation may also impact how you manage your finances. Your life stage can also inform and impact your time horizon and how you might invest or spend your money.

The amount that you invest, and how you choose to deploy your money, depends on your objectives, available funds and risk tolerance. Regardless of how you choose to invest, it’s important to take into account the various tax efficiencies that come with investing in different tax wrappers.

Get the balance right between ISAs and pensions

The choice between investing in an Individual Savings Account (ISA) and a pension can loosely be viewed as a trade-off between liquidity and tax relief. It’s generally a good idea to make use of both tax wrappers, which can help to fund your short, medium and long-term objectives. You should also periodically review your risk appetite for investing to ensure that you’re putting your money to work while also able to afford investing regularly.

Younger people typically have a greater need for liquidity than older people. Spending outlays like a house deposit require access to funds that are more readily available via an ISA than a pension. This is partly because you can take money out of an ISA at any age (subject to any specific withdrawal restrictions on that ISA), whereas you can’t access your pension until the age of 55. This threshold will rise to 57 on 6 April 2028.

Investing towards your retirement is important, but when you’re younger it’s usually not a good idea to ignore nearer-term liquidity needs to contribute solely towards a pension. Younger people may benefit from conversations with more experienced savers to help gain an understanding of how to manage their finances and how to get closer to achieving their financial goals.

If you are closer to retirement, reviewing your full financial position is sensible. Check whether your expected income stream, whether from pensions or other sources, is on track to deliver the amount of money you want in retirement. Depending on your situation, you may need to recalibrate assumptions about your retirement age and planned spending, or you might be ahead of where you had planned to be. Either way, you can then update your financial planning accordingly.

Whatever your financial objectives, investing via Direct Debit can help to ensure that you’re making regular contributions and spending time in the market, rather than trying to time the markets with one-off contributions.

Invest as early as possible

If you’re a seasoned investor, you could consider using your ISA allowance early in the tax year. Investing your annual £20,000 ISA allowance as early as possible can give your money more time in the market. If you already hold investments in a General Investment Account (GIA), consider selling and rebuying within your ISA to shelter future gains from tax. Unlike an ISA, with a GIA you pay tax on any returns.

If you need support with your financial objectives, you can book a free call with a J.P. Morgan Personal Investing wealth expert to explore how to set and meet some goals. If you’re looking for a personalised financial plan, we can also discuss if our paid financial advice might be right for you.

If you’re starting out on your investment journey or require a refresher on how tax wrappers work, we’d suggest that you read our guides on ISAs and pensions.

What to do now:

- Consider whether your financial goals are still the same as when you set them. Think about whether your priorities have changed, or if any of your goals have moved between time buckets.

- Compare how much you’re investing in an ISA with how much you’re contributing to a pension and make sure that you have the balance that works for you.

- If you have any questions or concerns, speak to a J.P. Morgan Personal Investing wealth expert.

2. Do you have enough cash?

It’s usually a good idea to think about building a cash buffer that you can use to cover unforeseen expenses and short-term spending needs. It’s worth periodically reviewing this buffer and assessing your standard monthly expenditure to ensure that you’re able to maintain it.

We typically recommend enough to cover three to six months’ essential expenses in an easy-access account. If your buffer has grown above this, could you reduce this buffer and increase the amount that you invest? Your personal circumstances will dictate the amount of emergency cash that you might need. The size of your cash buffer might also be informed by your proximity to your financial goals. It’s worth noting that J.P. Morgan Personal Investing does not offer easy-access accounts.

Avoid having too much of your wealth in cash

It’s important not to have too much of your wealth kept in cash once you have allowed for the above, for a couple of reasons.

Inflation: Many adults in the UK hold an excessive portion of their wealth in cash, which can leave savings vulnerable to the impact of inflation.

Taxation: The tax regime can be particularly punitive on people who keep excessive amounts of their savings in regular cash savings accounts. For example, a higher-rate taxpayer earning 4.5% annual interest on cash held in a savings account keeps a surprisingly low proportion of that return after tax. This is because higher-rate taxpayers only have a Personal Savings Allowance (PSA) of £500, which is the limit on tax-free savings interest each tax year. Once interest exceeds this threshold, every pound of interest is taxed at 40% (a higher-rate taxpayer’s income tax rate).

Cash can be held in a Cash ISA, where any interest earned is tax-free. However, if you are aged 64 or under, the amount of money that you can contribute annually to a Cash ISA will drop from £20,000 to £12,000 from 6 April 2027. Please note that J.P. Morgan Personal Investing does not offer Cash ISAs.

By contrast, the government has not announced any plans to reduce the £20,000 annual ISA allowance for Stocks and Shares ISAs, so you can still invest this whole amount into a Stocks and Shares ISA after March 2027 and your investment returns will remain tax-free.

With investing, it’s worth remembering that the value of your portfolio can go down as well as up and you may get back less than you invest.

What to do now:

- Confirm how much cash you have and check it against your recent spending. Does it still equate to three-to-six months of expenses and any short-term financial outlays you have planned?

- If you have accumulated cash above this level, you could consider increasing how much you invest while ensuring that you have enough to live off.

3. Could you increase your pension contributions?

Think about your salary and potential bonus for the year when planning how much to contribute to your pension. Could you contribute more? Your contribution rate should be set against a realistic view of your income and your expenditure.

If you’re in a workplace pension scheme, check the contribution rates offered by your employer and consider if you can increase your contribution level to make more of your annual allowance, and therefore benefit from more government tax relief.

You can use our pension calculator to help give you a clearer idea of how much you might need to contribute to reach your ideal retirement income.

Pension contributions can be used to reduce the amount of tax that you might pay on your income, as well as the tax paid by your partner. This amount is net of basic rate tax relief.

Pensions tax relief for employees works differently depending on whether you are in a ‘net pay' arrangement – where your pension contribution is deducted from your pay before the tax on your pay is calculated – or if you are in a ‘relief at source’ arrangement, when your pension contribution is deducted from your pay after tax. In a relief at source setup, this amount is net of basic tax relief which your scheme will claim from HM Revenue & Customs.

In a net pay arrangement, you don’t need to do anything to get your pensions tax relief. In a relief at source arrangement, basic rate taxpayers don’t need to do anything, but higher and additional-rate taxpayers will need to claim their tax relief, typically via a self assessment tax return.

You can read more about how tax relief on pension contributions works in our Pensions and retirement guide.

Sacrifice salary to beat the 60% tax trap and unlock free childcare

Pension contributions can be used under ‘salary sacrifice’ arrangements to help to mitigate against the impact of the so-called '60% tax trap'. A quirk in the tax system means that anyone earning between £100,000 and £125,140 can find themselves paying an effective tax rate of 60% on this portion of their earnings. This is because when your taxable income is over £100,000, your £12,570 tax-free personal allowance tapers away at a rate of £1 for every extra £2 you earn.

In practice, this means that for every £100 of income you earn between £100,000 and £125,140, you only get to take home £40. This is because £40 goes to higher rate income tax, while another £20 is lost due to the tapering of the personal allowance. If your taxable income is between £100,000 and £125,140, sacrificing salary in favour of pension contributions can prevent this income from entering a higher tax bracket.

This arrangement can help people access free childcare. In the UK, if one parent’s expected adjusted net income is over £100,000 for the current tax year, their child is not eligible for 30 hours’ free childcare per week. Using pension contributions to reduce your salary can therefore unlock this benefit.

It’s worth noting that from April 2029, only the first £2,000 of employee pension contributions through salary sacrifice every year will be exempt from National Insurance contributions (NICs).

Check whether you have unused allowances

It can also be a good idea to make the most of ‘carry forward’ rules where possible, which allow you to make pension contributions from unused portions of your annual allowance for the previous three tax years, as long as you were a member of a pension scheme during those years. To use carry forward, you must make the maximum allowable contribution in the current tax year, after which you can then use any unused annual allowances from the three previous tax years. When you have used your allowance for the current tax year, any unused allowance in the earliest tax year available is used first.

It’s important to remember that you’re not able to receive tax relief on personal contributions in excess of your relevant earnings in a tax year, and you’ll only receive higher rate or additional rate tax relief to the extent you’ve paid the higher rate of tax. The annual allowance for pension contributions rose from £40,000 to £60,000 in April 2023. Your relevant earnings are income that is eligible for tax relief, which includes employment income.

Pay into your partner’s pension to increase your household savings

Finally, if you have a partner, paying into their pension can be a smart move for the new tax year. You can pay up to £2,880 per tax year towards the pension of a non-earning person aged under 75, who will receive a government top up of 20% via tax relief. The government top-up takes this total contribution up to £3,600.

If the recipient is working, the amount that you can pay into their pension is capped at the annual allowance of £60,000 or 100% of their earnings per tax year, whichever is lower. Your contributions must remain within your partner’s annual pension allowance to ensure that this payment does not incur a tax charge. Please note their pension allowance may be tapered if they are a very high earner, and that they need to be under the age of 75 to get tax relief.

Paying into your partner’s pension might also help to reduce the Gender Pension Gap.

It’s worth noting that you cannot pay directly into your partner’s J.P. Morgan Personal Investing Personal Pension from a bank account that does not have your partner registered as one of the named holders of the account. If you have a joint bank account with your partner, you can use this account for contributions into a Personal Pension. J.P. Morgan Personal Investing only collects pension payments via Direct Debit. You can therefore pay into your joint bank account and use this account to contribute towards the funds that we collect via your partner’s Direct Debit mandate with us. You can alternatively gift the money for them to contribute into their pension. Gifts between spouses or civil partners are not taxable.

If you’d like to know more about investing tax-efficiently, you can read our guide on the subject.

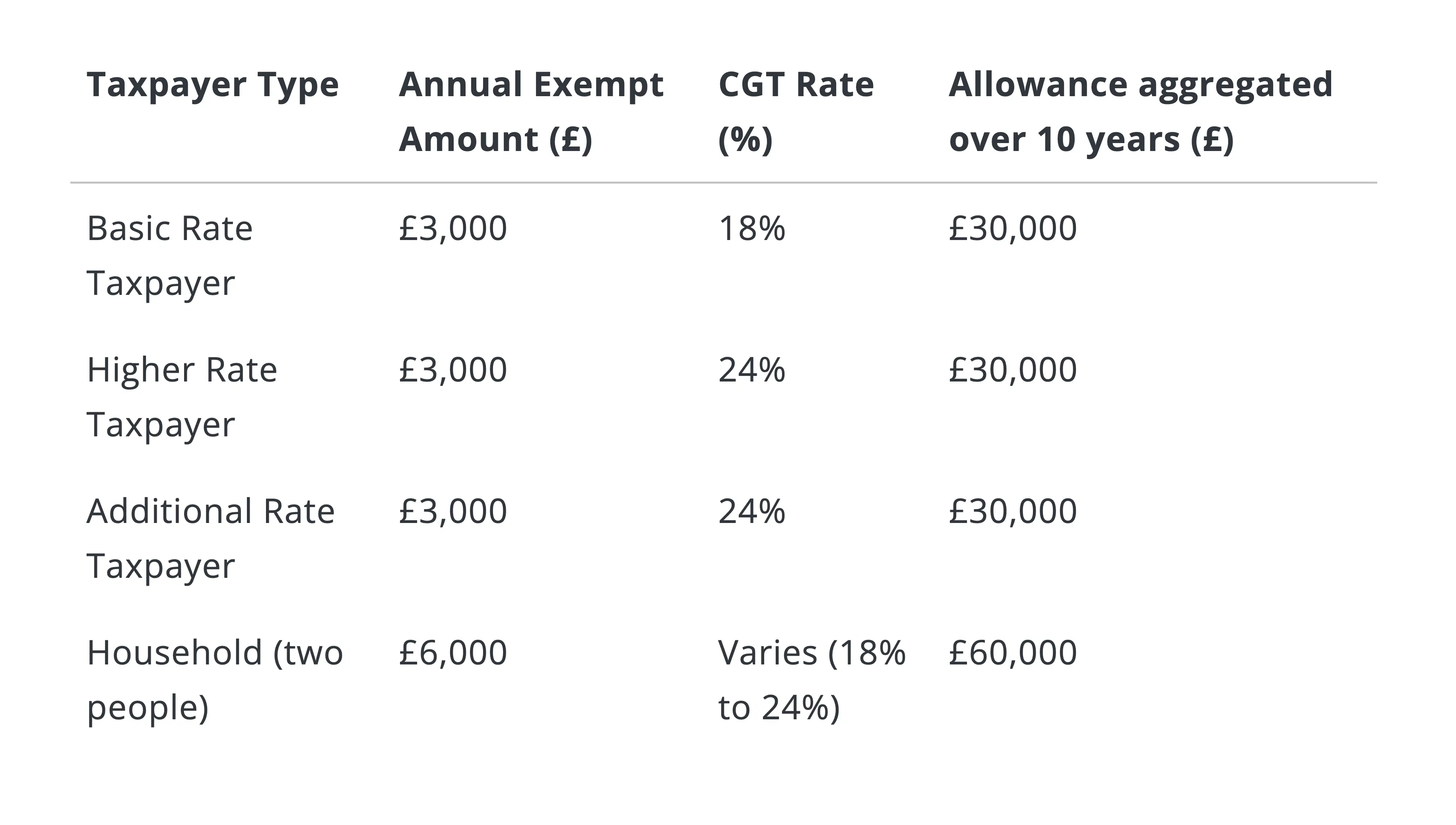

4. Use your Capital Gains Tax allowance

An individual can make total gains of £3,000 per tax year on assets they have sold or ‘disposed’ of before they pay Capital Gains Tax (CGT). This is referred to as the Annual Exempt Amount. You can read more about CGT in our guide to tax-efficient investing.

There are several measures that you can take to reduce your CGT liability, including maximising the use of your tax wrapper allowances. Investment returns generated in an ISA or pension are not subject to CGT, while CGT is levied on investments in a GIA above the tax-free CGT Annual Exempt Amount.

Plan your disposals across tax years

Selling all your investments at once is usually not tax-efficient. Consider instead spreading disposals across multiple tax years to use your £3,000 allowance each year. Over 10 years, a two-person household has a combined CGT allowance of £60,000, but only if you actively plan to use it each year.

What to do now:

- At the start of each tax year, consider whether you want to sell any of your investments at all.

- Once you’ve done this, review your GIA holdings and identify how much of your £3,000 allowance that you might want to make use of.

- Start thinking about the bigger picture and create a disposal schedule to make the most of your allowance over the long term. Consider conducting a ‘Bed and ISA’ transfer, which involves moving investments that you own outside your Stocks and Shares ISA (for example, in a General Investment Account) into this tax-efficient wrapper. If you plan to make the most out of a Bed and ISA strategy, weigh how paying a bit more in CGT today might compare to the longer term tax savings of Stocks and Shares ISAs.

- If you have a spouse and you live together, transfer assets between you before you sell them, so you can both use your individual £3,000 allowances. You won’t incur CGT by transferring assets to your spouse.

You can read more about CGT in our guide to tax-efficient investing.

Speak to our wealth experts

Our wealth experts can help you explore how you could invest more tax-efficiently while making the most of your annual allowances.

We can work with you to explore your options, answer questions and discuss how you could use a combination of investment products. You can book a call to speak to one of our experts for free.

If you would like a personalised financial plan, we also have paid financial advice where we will review your finances and goals to help you build a financial plan with our recommended approach for you.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. Tax rules vary by individual status and may change. This is general information, not personalised tax advice. We provide 'restricted advice', meaning we only make investment recommendations on the products and services that we offer. Seek financial advice if you're unsure if a pension is right for you.