Investing throughout your lifetime

Managing your wealth is a lifelong journey. This guide explains how a qualified wealth manager could help to break it down into the milestones that are right for you.

Author: Andrew Lacey

This page was last published on 3 November 2025.

At a glance

- Wealth can be daunting to think about, no matter what stage you are in life. Viewing your relationship with wealth as lifelong, but broken down into various moments and milestones, can help – especially with a qualified expert like one of our wealth managers to offer you guidance or advice.

- Understanding the account types available to you – including tax wrappers – can help you to maximise your wealth potential.

- A wealth manager can help you balance your longer-term wealth goals with your shorter-term financial needs, and guide you towards the appropriate amount of risk to take on.

- Money milestones are different for everyone, and there is no predetermined map for long-term wealth. Adopting a positive ‘outcomes’ mentality can add much-needed flexibility into a robust financial plan.

Building long-term financial prosperity is a lifelong process, similar to maintaining good health.

Building a stable financial future is not, with some lucky exceptions, something that can be achieved in one go. Some successes or setbacks might be specific to certain phases of life, but financial decisions can rarely be made in isolation.

This guide takes a look at some key life moments, the big financial milestones many of us will aim for on our lifelong wealth journey, to illustrate how your own long-term financial plans might shape up. The guide then explains what you can expect from your relationship with your wealth manager, if you choose to use one, including the types of information they may ask for, and why it is important for them to tailor the guidance or advice you receive.

Outcomes are more important than age

It can be tempting, when thinking of wealth, to focus on what you 'should have achieved' by a certain age. Everyone's circumstances differ though, and the financial goal that is right for one person might not be appropriate for another.

The investment horizon for a 30-year old, for example, may on the face of it be longer than someone closer to retirement, but it depends on their more immediate ambitions. While a 50-year old investor might be closer to retirement, the 30-year old might need access to some or all of their money much sooner to buy a home.

Your wealth manager should factor in where you are, and where you want to be, and should focus on positive outcomes. Life stage is certainly an important consideration when managing your finances, but it shouldn't overshadow all other factors.

Niraj Madlani, Senior Wealth Manager at J.P. Morgan Personal Investing, explains:

"We look to understand what is most important to our clients and give them a clear path towards achieving their goals. We want to develop a client’s understanding of financial planning so they can make an informed decision. A guidance call typically lasts anywhere between 30 minutes to an hour. A lot of clients can have successful outcomes through guidance, but throughout the call, the agent will typically establish whether paying for advice would be a more suitable option. From that point, our clients typically have a direct line of contact with the Wealth Services agent given they have built a relationship.”

One of the first questions our wealth managers will typically ask is how long you want to invest for. They may then follow up with some questions that check the first answer ties up with other details you provide:

- Are there any expenses or outgoings you might anticipate for the next few years?

- Do you need your money to be accessible?

- Do you have cash in reserve for known outgoings, and a buffer for the unexpected?

The advisers at J.P. Morgan Personal Investing would typically caution against investing in financial markets – via stocks and bonds – if you think you will need your money within three years.

Tax rules vary by individual status and may change. We provide 'restricted advice', meaning we only make investment recommendations on the products and services that we offer.

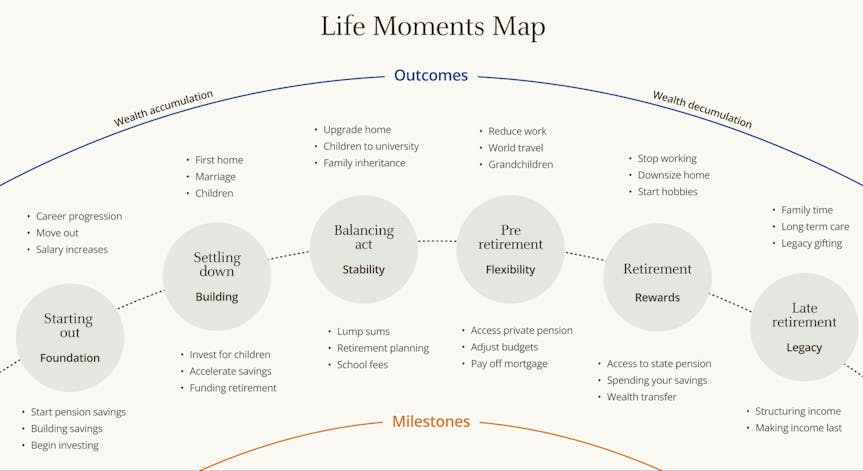

Life moments: your wealth journey's milestones

This section of the guide explains the practical ways the information gathered through the fact finding conversations with a wealth manager can be put to work. Below are examples of milestones that most people will consider during their lifelong wealth journey, and some of the nuances around them.

Source: J.P. Morgan Personal Investing. This is for illustrative purposes only and is not advice.

Life doesn’t play out in a neat infographic: you might have some, but not all of these outcomes in mind, and perhaps in a different order. Below we elaborate on some of the common milestones and how you can set yourself up to reach them.

Starting a pension

Getting a pension up and running is a sensible financial priority for almost everyone.

According to the Office for National Statistics, the average British woman lives to be (almost) 83, while the average British man should live to around 79. This means if you retire at 60, on average your pension savings would need to last you 20 years or more. The base assumption of the J.P. Morgan Personal Investing pension calculator is for retirement to last 20 years, but your pension may well need to support you for longer. Combine this with the Pensions UK estimate that a retirement of 'moderate' comfort requires an annual income of around £31,700 for one person, and the case becomes strong for starting as early as possible.

Starting early is one of our key investing principles. It can maximise the potential impact of compounding to increase the likelihood you will meet your financial goals. Starting to contribute to a pension early also means that any sums you regularly set aside for your pension can be lower, and therefore consistent. Starting later might mean you’d need larger contributions, which are harder to maintain at the same rate.

Senior Wealth Manager, Niraj Madlani, explains:

“Money can’t buy time, but it definitely can buy flexibility. Putting aside an affordable and sensible amount into a pension early on means you do not have to sacrifice on things later on. You also get the immediate benefit of reducing the amount of your income that is taxable.”

Pension contributions are treated favourably by the UK government from a tax perspective, whether via a workplace pension, or a private pension. This means your savings are immediately worth more in a pension than in your personal bank account, due to tax relief, which means the government will add to your pensions based on how much income tax you pay. That's before we factor in the potential returns from long-term investment.

As Niraj says, it's all about increasing your options:

“One of the key things I get my younger clients in particular to think about is what type of retirement lifestyle they would like to live. Give yourself plenty of opportunity to make your ideal retirement a reality – whether that is going on several holidays per year or sitting comfortably at home.”

*From April 2029, contributions to pensions via salary sacrifice over £2,000 per tax year will no longer be exempt from NICs.

Investing flexibly

Stocks and Shares ISAs are the most popular account type we manage at J.P. Morgan Personal Investing, for a good reason.

While pensions are usually the main way that most people save for retirement, ISAs can also be an excellent investment tool for both the long and the shorter term. One advantage they can generally offer is a higher degree of flexibility than pensions when it comes to accessing your money. This can make them a valuable tool when making plans for life events with more flexible timings, such as:

- Renovating your home

- Supporting a growing family

- Exploring an opportunity to travel

We have a dedicated Guide to ISAs here, which provides important details including ISA types, annual allowances, and how personal ISAs differ from Junior ISAs (JISAs).

Buying a first home

Saving up for a first home can be difficult. Between other outgoings and pension contributions, putting money aside for a house deposit can feel like a battle.

J.P. Morgan Personal Investing typically suggests that investors should expect to leave capital invested in financial markets for around three to five years (as a minimum). This is because the value of investments can move around, especially in the short-term, which may impede an investor’s ability to follow through on a property purchase. This should be factored into any decisions to invest in stocks and bonds when building a house deposit.

A Lifetime ISA (LISA) can be a useful product when saving for a first home, and may be something you discuss with your wealth manager in these circumstances. LISAs are available to open for those aged 18 to 39, who reside in the UK or are a member of the armed forces or a crown servant (or their spouse or civil partner) if you do not live in the UK. You can continue paying into a LISA until your 50th birthday. Crucially, contributions into a LISA benefit from a 25% government bonus, up to a maximum £1,000 per tax year, which is paid when you contribute (up to the maximum £4,000 LISA allowance per tax year). The £4,000 LISA allowance counts towards your £20,000 annual ISA allowance.

LISAs are designed specifically to aid investors in saving for a first home or to build towards retirement, and you can only use it for these two purposes. You can only access the money in a LISA either to buy your first home – up to a cost of £450,000 – and for retirement purposes once you’re 60.

Investors should be aware that you can access LISAs if you’re terminally ill, with less than 12 months to live, but if you need to use it for reasons outside these criteria, you’ll have to pay a government withdrawal charge of 25%.

There are two types of LISA. Stocks and Shares LISAs invest in financial markets and provide tax-free returns, while cash LISAs are tax-free savings accounts. J.P. Morgan Personal Investing provides a Stocks and Shares LISA, but does not offer a Cash LISA. As mentioned earlier, there may be some investors for whom a Stocks and Shares LISA is not appropriate, if for example, their plan is to use the funds to buy a home within three years. If that is the case, and you decide that a Cash LISA is more appropriate, you can still benefit from the 25% government bonus.

Funding university

The costs associated with pursuing further education can be substantial, but by planning ahead, you can help your children get a head start.

The yearly cost of university tuition is capped for home students in UK universities, at £9,535 for a standard full-time course (2025/26). From 2026 they will increase annually, in line with inflation. This is before other living costs, which can vary significantly depending on – amongst other things – where the course takes place.

Your child may not want to attend university, but using a JISA to build up a pot over time can help to keep the option on the table for them, and it can of course be used to support them in pursuing other further education, apprenticeships, covering living expenses or however they wish.

The annual JISA allowance (£9,000 per tax year) pertains to the beneficiary (the child for whom it is invested). It is distinct from the annual ISA allowance for individuals and does not contribute to an individual's annual ISA allowance.

A JISA is a tax-free savings account set up by a parent or legal guardian for a child. The account holder pays no tax on interest, capital growth or dividends in respect of any contributions up to the Junior ISA allowance. The JISA is essentially an amended version of the adult ISA, but with a lower £9,000 annual limit, and different restrictions on withdrawals.

Government guidelines state the child needs to be below 18 to open a JISA. The J.P. Morgan Personal Investing JISA can only be opened for children below 16 years of age. A child can have one Stocks and Shares JISA and one Cash JISA. If you have multiple children, you can open a Cash JISA and a Stocks and Shares ISA for each of them. However, J.P. Morgan Personal Investing only offers a Stocks and Shares JISA.

Anyone can contribute to the account, but only the child can access the money – and only after they turn 18.

Approaching retirement

Building a pension to support a comfortable retirement is a key element of most people's financial plans. As you approach retirement, guidance or advice from a wealth manager can come into its own when tailoring a drawdown strategy to your needs.

You don’t have to take your pension all at once. Many people opt for 'drawdown' which means you can withdraw money as you need it (at an appropriate rate), while leaving the rest invested for the future. Most people can take 25% out of their pension tax-free, with subsequent withdrawals taxed at your marginal rate of income tax. This 25% is typically subject to a lump sum allowance, which is currently £268,275. You can also choose to buy an annuity, which gives you a secure income for life, but lacks the flexibility of drawdown. Each route has its pros and cons, so it’s worth considering what fits your plans.

We have written a dedicated Guide to Pensions and Retirement, should you want more information.

Planning for retirement is an exciting phase of your wealth journey. Your capacity to reduce your working hours, or stop altogether, may mean you can travel more, pursue hobbies or spend more time with family, such as grandchildren.

As Senior Manager and Financial Planner Holly Graham explains, your wealth manager can clarify the options available to you and help ensure you’re making the most of your pension pot:

“Investors can, but don't need to, take the full 25% lump sum in one go. You can phase it over many years in order to maximise retirement income. This is an approach that could lead to a better retirement outcome over time, meaning more money to spend than if taken in one go.

“It is called phased drawdown. We see clients taking a combination of income and tax-free cash each tax year between leaving work and the state pension age. Managed correctly, combining pension income and some of your tax-free lump sum can mean all income could fall in the 0% tax band of the personal allowance.”

Thinking about how long you’ll need your pension to last is important, and may feed into when you choose to fully retire. We’re all living longer, and inflation means things get more expensive over time, so some investors may favour a reduction in hours before stopping work entirely. Again, these are questions you might be asked by your wealth adviser to help you decide things like a sustainable rate of withdrawal.

Balancing long-term care and legacy

Most if not all of the wealth planning milestones discussed here can contribute to the wellbeing of loved ones. A complete wealth plan can support them more directly, by providing for your family, friends or causes that matter to you, after you've gone.

We have written a dedicated Guide to Leaving a Legacy if you would like to find out more.

Considerations for what you can pass on should not take precedence over your own financial wellbeing. Indeed, considering healthcare costs, and how you might pay them is another planning step that could reduce any burden on your family at a challenging time.

Holly Graham explains long-term care costs can increase in phases, but can be considerable:

“The need for care – and care costs – tends to rise very gradually. It may start with family members helping, which is usually free. An older person may then need adjustments to their home, such as a handrail in the shower or a stair lift, which are expenditures, but relatively contained. A professional at some point may need to attend the home a couple of hours a week, before ultimately an older person may need to move into full residential care. This can be expensive – between £800 to over £1,500 per week – which is why we model care costs as part of our paid-for advice service.”

Late in life, your wealth adviser can help you figure out where you stand when it comes to gifting wealth and how the transfer of wealth may unfold after death. Paired with your Will, this phase of your wealth planning can ensure clarity in the process of distributing your estate. And while J.P. Morgan Personal investing does not provide tax advice, your wealth adviser can help you understand the tax-efficient vehicles available that can improve inheritance tax efficiency.

“Considering your legacy is incredibly important and can be life-changing,” explains Niraj Madlani. “By very clearly expressing your wishes for your estate, you can minimise tax, reduce any legal costs, prevent any unwanted disputes, and ensure that your hard-earned estate goes to what matters most to you, such as your loved ones or any charities.”

Tax rules vary by individual status and may change. We provide 'restricted advice', meaning we only make investment recommendations on the products and services that we offer.

How a wealth manager can help you

Considering a lifetime of financial goals can be overwhelming. That's why it can often be helpful to speak to a qualified wealth manager, who can ask you the right questions to help you build up a clear picture of your full financial position, and set you on a path to achieving your future goals.

Guidance vs. advice

Qualified wealth advisers, such as our wealth managers, can provide helpful general guidance, or tailor their advice based on individual circumstances. A good relationship with a wealth adviser may last many years.

J.P. Morgan Personal Investing offers both financial guidance and restricted advice.

Guidance is a free service, offering a general overview of how investing works and which products could be the right choice, but will not factor in your personal circumstances.

Advice is a paid service that will involve fact-finding conversations with your wealth adviser in order to provide recommendations that are tailored to you. J.P. Morgan Personal Investing provides 'restricted advice', which means we will only make investment recommendations on the products and services that we offer.

You might start with a free financial guidance call, and decide to go on to use the paid-for advice service.

Understanding the role of different account types

Knowing the types of accounts you might use through your investment journey, and how they differ, can be very valuable in forming long-term plans. Whether you are receiving financial guidance or tailored advice, your wealth manager may spend some time explaining the characteristics of each.

Individual Savings Accounts (ISAs) are popular, and come in several forms. A Stocks and Shares ISA allows investors to invest in financial markets, with returns sheltered from tax, subject to the investor contributing no more than their annual allowance. Cash ISAs offer tax-free interest on savings. Lifetime ISAs (LISAs) provide a government bonus to help savers buy a first home or retire. They can be opened by UK residents aged 18-39, and contributed to until age 50. Junior ISAs (JISAs) enable parents and legal guardians to save tax-free for children under 18 (anyone can also contribute once open).

We have written an extensive guide on ISAs here.

For those seeking greater flexibility, General Investment Accounts (GIAs) do not limit how much an investor can contribute each tax year. While they do not offer all the tax advantages of ISAs or pensions, Senior Wealth Manager and Financial Planner Holly Graham explains they can still be valuable tools.

“I consider a GIA to be a useful product to use other allowances and exemptions that an investor may not be using on an annual basis, such as the Capital Gains Tax (CGT) exempt amount and dividend allowance. Tax rates for CGT and dividends are generally lower than that of income tax, so for some, using a GIA can provide a more tax efficient route than a high interest savings account, albeit with different risk of loss.”

Pensions, including workplace pensions, personal pensions, and Self-Invested Personal Pensions (SIPPs), offer tax relief on contributions and are central to long-term retirement planning.

Each account type is designed to suit different financial goals and circumstances.

Access, income and tax efficiency

If a client believes investing is right for them, the next step in the conversation might involve a few questions around income, as well as existing savings and investments.

Investing as tax efficiently as possible can make a huge difference to your outcomes and the likelihood of you meeting certain goals. Information you can give your wealth adviser on income from employment and any other sources, as well as investments elsewhere, can help you do this.

For example, according to the Office for National Statistics, most people's earnings peak at about 47 years old. Changes to earning power over your career mean adjustments to what you save towards retirement – up or down – may be appropriate. In addition to bringing you closer to a comfortable retirement, pension contributions can help bring your income tax bill down for those caught by personal allowance tapering or those in higher or additional rate tax bands.

Of course, pension savings are not in most cases accessible until you are of retirement age, and there are plenty of reasons an investor might need access to their funds before then.

For many investors, it is also often a good idea to make use of your ISA allowance to the extent that you can afford (up to an individual's maximum annual allowance of £20,000). Contributions to ISAs do not offer tax relief the way pension contributions can, but using an ISA still shelters any capital gains, dividends and income from tax, while keeping it more accessible if it is needed.

Risk appetite vs risk capacity

Risk is often misunderstood in the context of investing and building wealth.

In the case of investing, it carries numerous meanings and can be measured in numerous ways. One of the most common methods of expressing investment risk is to indicate how much the value of your investments is expected to move around in a given period. This is called 'volatility'.

This measure of risk is based on past performance data, and therefore cannot guarantee future results. However, in general, a higher risk portfolio may be expected to see both the value of investments fluctuate more over the short term than a lower risk portfolio, and produce higher returns over the long term.

Investors who don’t mind seeing bigger moves in the value of their investments (up and down) would be considered as having a higher risk appetite. An investor less comfortable with these movements would be considered to have a lower risk appetite. Your wealth adviser can help you understand how your risk appetite compares with your risk capacity (how much risk you can financially afford to take). This can involve adequate cash buffers, but is a result of numerous factors.

Some investors may consider themselves to have a low risk appetite but have greater capacity for risk than they realise. Others may have a high appetite for risk, but may have a lower risk capacity than they realise. For example, an investor may have limited time until they need to draw down on their portfolio.

In the context of retirement planning, the reduction in portfolio risk as an investor nears the point that they will need to rely on a portfolio is often called 'lifestyling'. It is a gradual process, usually undertaken over several years, that can shift a portfolio's balance away from higher-risk asset classes (like equities), into historically lower-risk asset classes (like government bonds).

Essentially, an investor's risk appetite may remain fairly steady throughout their lifetime, but their capacity for risk may change. This is something that your wealth adviser will help you to understand.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. Pension/ISA/JISA/LISA eligibility rules apply. With LISAs, govt withdrawal charges may apply. Seek financial advice if you're unsure if a pension is right for you. Tax rules vary by individual status and may change. This is general information, not personalised tax advice.

We provide 'restricted advice', meaning we only make investment recommendations on the products and services that we offer.