ISA contributions: When should you contribute to your ISA each year?

Andrew Lacey

7 min

We crunched the numbers and found that investing in your ISA earlier in the tax year – or regularly throughout – could potentially improve long-term returns, when compared to holding off until the end of the tax year to make ISA contributions just before the tax year end.

At a glance:

- Many UK tax allowances are “use it or lose it” each year. Because unused ISA, LISA, and JISA allowances expire at the end of the tax year, many investors wait to top these up in late March, or early April. But does this make the most of your available tax allowances?

- Our calculations suggest that drip‑feeding your Stocks and Shares ISA contributions through the tax year, and contributing earlier in the tax year, could improve your long-term returns compared to investing at the end of the tax year.

- If you want to use your allowances but are not sure about the timing or how to approach this, our team of wealth experts is here to help

Investing in a Stocks and Shares ISA earlier in the tax year could improve returns

Our clients often ask our wealth experts when they should invest, and if their timing matters throughout the tax year.

We always advocate for time in the market instead of timing the market, meaning that if you invest for long-term goals you should not be too concerned with picking the perfect day or month to top up your ISA or start investing.

Investing is subject to the ups and downs of financial markets, and there’s a risk you’ll lose some or all of the money you’ve put in, so returns aren’t guaranteed. However, by investing over the long-term, you can give your investments time to make up for any short-term losses.

If you are concerned about market performance, drip-feeding your money can help you average out the impact of market movements, a concept called pound-cost averaging. Investing a lump sum means investing all of your contribution in financial markets at the same time.

As a reminder, you can pay into a J.P. Morgan Personal Investing ISA to use your annual allowance and if preferred, keep the money in cash at first, and drip feed it into markets over time.

That said, analysis undertaken by our investment team looking back over the past 10 tax years suggests that investing in markets at the start of a tax year, throughout the year, or at the end of the tax year could have an impact on your ISA’s long-term returns.

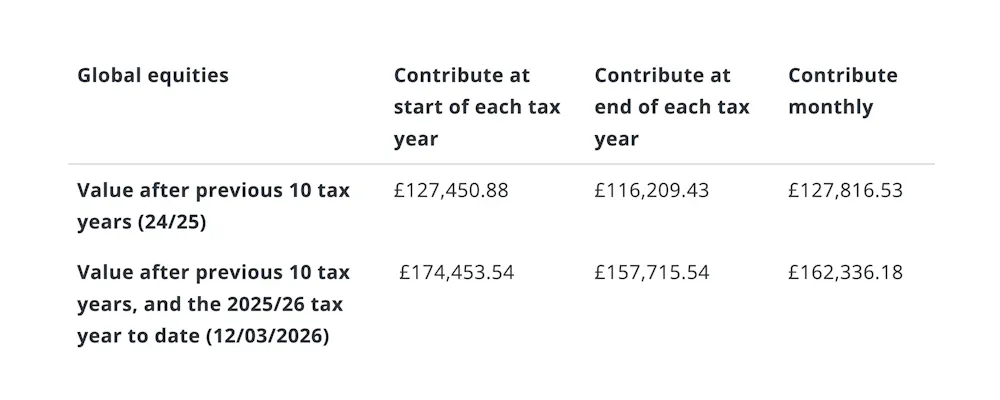

Our research suggests that if you had started investing the average annual ISA contribution (£7,594) into your Stocks & Shares ISA from the 2015/16 tax year until March 2026, you would now have £162,336 if you drip‑fed money equally into a global markets tracker each month.

Investing the same annual amount as a lump sum at the start of each tax year would have resulted in £174,453. By contrast, the calculations suggest you’d have a sum of £157,715 if the lump sum was invested at the end of the tax year.

Note: These figures are based on the past performance of one particular index. This does not indicate how your own investments will perform, and past performance isn't a reliable indicator of future performance. Always invest in a way that works for you.

Source: J.P. Morgan Personal Investing, as of 12 March 2026. Global equities data is based on the MSCI All Country World Index. The average Stocks & Shares ISA contribution of £7,594 is for illustration only, drawn from the latest available HMRC analysis on ISAs (for the 2023/24 tax year, in the September 2025 report). These figures refer to past performance, which isn't a reliable indicator of future performance.

Should I invest at the start of the next tax year?

Investment Strategist, Scott Gardner, says: “Investors who begin investing early in the tax year can benefit from having their funds in the market for longer compared with those who wait until the final weeks of the tax year.”

While many people focus on last‑minute tidy‑ups, the data suggests that thinking about contributions towards the beginning of the tax year may also be worthwhile.

“Those who opted for an early lump sum investment have seen their wealth grow more, based on historic data,” says Gardner.

“While we would never suggest trying to time the market, we do advocate giving your investments time in the market. Long-term investing increases the probability of generating profits and allows more time to benefit from compounding, in a tax-free environment.

“Making monthly contributions into your Stocks & Shares ISA has the benefit of drip-feeding money into financial markets which can help smooth out any periods of volatility, as we have seen recently and in the past, when the pandemic impacted global markets.”

Should I still maximise my contributions at the end of the tax year?

If you don’t have cash available to invest at the start of the tax year (6 April), the principle still holds that the earlier you invest the longer your money has to benefit from compounding and time in the market.

Rather than waiting until the end of March next year to make a start on your ISA contributions, you could either drip feed small amounts throughout the year, as explained above, or make a habit of reviewing your finances regularly, for example, each quarter, to see if you are in a position to invest.

Before putting your money in an ISA and investing in financial markets, always check first that you have cash available to meet your short-term needs. Keeping a cash buffer outside of an ISA (such as in a regular savings account) can help you meet planned and unplanned life events in the short term, and is one of our investment principles.

Once you’re comfortable that you have this buffer, you can work out how much you can afford to contribute to your ISA. If you are in a position to contribute, and have remaining allowances, the tax efficiencies offered by ISA accounts mean you can keep more of any gains you make (which can be taxed in some other types of account).

The lead up to 5 April each year still remains a good time to check over your finances and, if you can, use any remaining annual tax allowances, including your ISA allowance.

Some annual allowances only apply to a given tax year, so any of that year’s allowance that you don’t use may be lost. For example, while pensions typically allow you to carry forward unused allowance from the last three tax years, this is not the case for ISAs, Lifetime ISAs (LISA) or Junior ISAs (JISA). Investors might therefore want to top these ISAs up by the end of the tax year to take advantage of any tax-efficiencies.

Ready to invest but not sure how?

If you know you want to open or contribute more to a Stocks and Shares ISA but are not sure exactly how you want your money to be invested, you can book a free call with a member of our wealth team to discuss your goals and what risk level and investment style might be appropriate for you.

Book a call with our wealth experts

It’s also worth noting that you can set up multiple pots for different goals, including a cash pot if you need more time beyond 5 April to decide on how you want to invest. It’s important to note that a cash pot is not a Cash ISA, and is intended to be used to hold your money within your Stocks and Shares ISA in the short term, before you decide on an investing style, J.P. Morgan Personal Investing does not offer Cash ISAs.

For anyone who needs a refresher, you can brush up on your knowledge of the annual allowances available to you, and a range of other wealth information, with our detailed guides.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Tax rules vary by individual status and may change. Pension/ISA/JISA/LISA rules apply. J.P. Morgan Personal Investing does not provide tax advice. For personalised advice tailored to your specific situation please consult with a qualified tax adviser or financial planner.