Preparing for tax year end: the dates you need to know

It is never too early to get your finances organised. Here we explain the key dates you should be aware of as the end of the tax year approaches, using indicative dates from 2026. This article uses the dates from 2026, but we will update them in due course to reflect the 2027 tax year end deadline.

Author: Andrew Lacey, Co-Author: Navisha Joshi

Published on 23 October 2025. Last updated on 12 March 2026.

At a glance:

- What to do ahead of tax year end

- Deadlines for payment contributions with J.P. Morgan Personal Investing for the 2025/2026 tax year

- Please note these are not the dates for the current tax year. The 2026/2027 deadlines will be confirmed later in the tax year but are not likely to shift drastically. Clients will be informed of the confirmed dates closer to the time.

- The below is for your information only, to help you plan your tax year in advance.

What should I do before tax year end?

When does the tax year start and end? The tax year runs from 6 April to 5 April the following year.

As the end of the tax year approaches, there are a few things investors should have on their checklist.

- If you don’t have an ISA or pension, you can consider opening one or several to make the most of any tax allowances.

- Review your contributions into your existing ISAs or pensions this year, and check remaining allowances.

- Consider whether you can top up ISAs or pensions. You don’t have to maximise allowances to make a difference.

- Weigh up investing a lump sum and ‘drip feeding’ future contributions. You may, for example, have the funds available to use your full ISA allowance at the start of the tax year, but prefer add it to the market gradually. We explain this more below.

- Ask for help if you need it. The tax year end can be a busy time, and tax can be complicated.

Leaving yourself plenty of time to invest before the end of the tax year on 5 April 2026 means you can avoid any last-minute worries and make the most of your tax allowances.

How can I invest this tax year?

There are a variety of ways to contribute and invest your money. Further down we explain the mechanics of paying in by direct debit, debit card, easy bank transfer, manual bank transfer, Apple Pay, Google Pay and from your General Investment Account.

But before this, it’s useful to understand that you can either put your contributions directly into the market, effective as of the next J.P. Morgan Personal Investing trading cycle (detailed below), or you can choose to drip-feed your contributions into the market over time.

Investing in the market directly

When we receive your contribution, we allocate it to your account. If we know the destination pot, we will allocate the money directly to that pot. If we do not know the destination pot (usually when a client makes a manual bank transfer and has more than one pot in their account) then we will add the money to unallocated cash and you will need to log in and allocate funds to your chosen pot.

Once the money is allocated you will see it marked as ‘New cash to be invested'. We will invest this money during our next trading day (typically we trade twice a week). If, for instance, we receive money on Tuesday and the next trading day is on Thursday, the money will remain as ‘New cash to be invested' until Thursday, by the end of Thursday you will be able to see exactly what we bought in your ‘Investment Activity’.

Drip-feeding

'Drip feeding' is all about contributing smaller amounts on a regular basis – taking advantage of what investors call ‘pound-cost-averaging’ – and means you’re less exposed to short-term market movements.

The J.P. Morgan Personal Investing 100% cash pot feature works – in ISAs and GIAs – by connecting up two J.P. Morgan Personal Investing pots with a monthly transfer. You’ll need two pots – one will be a cash pot, and the other will be an investment pot. Money added to the cash pot with J.P. Morgan Personal Investing is not initially invested, but is instead transferred to the investment pot over time.

With ISAs this ensures the cash has the tax protections when it is ultimately invested. Please note the cash only pot option is not available for income investing pots.

As the J.P. Morgan Personal Investing Pension does not currently have a cash pot feature, you could act on the investment theory in the same way by setting up a monthly direct debit.

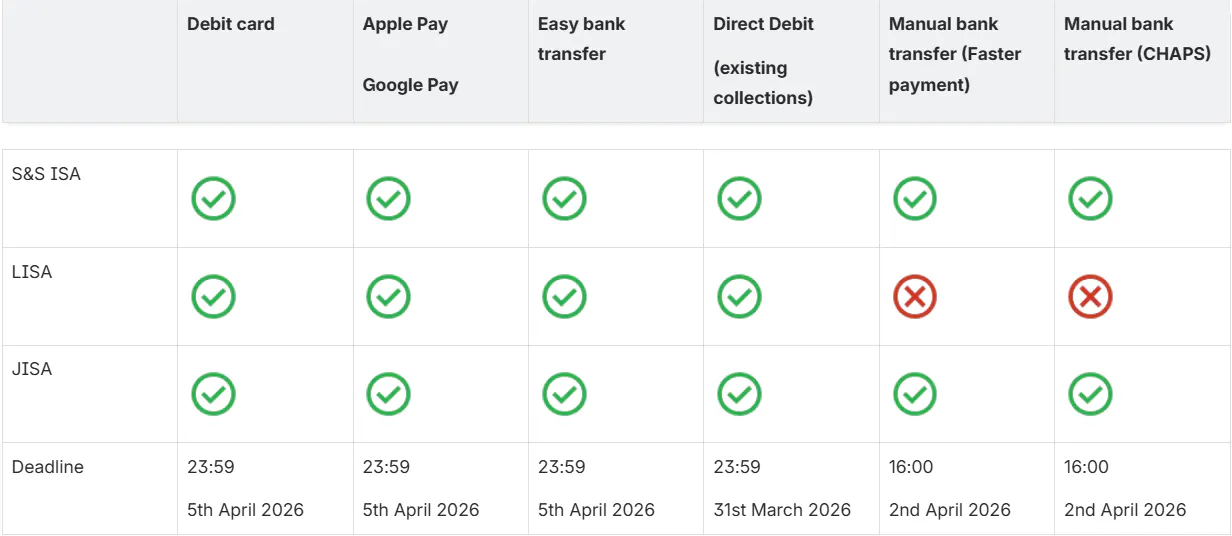

If you have a J.P. Morgan Personal Investing Stocks and Shares ISA, Lifetime ISA or Junior ISA

Key dates for contributions (indicative dates only)

Note: The dates provided here are for the end of the 2025/2026 tax year (April 2026). The 2026/2027 deadlines will be confirmed later in the tax year.

There are several routes to contributing to your Stocks and Shares ISA, LISA or JISA to make sure any money added is attributed to the 2025/26 tax year. You can contribute as many times as you like before the end of the tax year with any combination of lump sums and regular payments, providing you don’t exceed the annual allowance.

Regular contributions (indicative dates only)

Direct Debit

- If you make regular contributions via a Direct Debit that are collected from your bank account between 1-5 April, your Direct Debit contribution will not make it in time to count for the current tax year and will instead count towards your new 2026/27 tax year allowance. Therefore, you’ll need to cancel your existing Direct Debit and set up a new one so that it is collected on or before 31 March 2026

- Be aware that it typically takes up to 10 business days to set up a new Direct Debit. However, in certain cases a manual verification may be required which could extend the timeline by an additional five days. We therefore recommend allowing plenty of time and making any changes by 16 March 2026.

Standing order

- If you make regular contributions with a standing order, you’ll need to be on top of the deadlines for manual bank transfers.

- For most standing orders via Faster Payments the deadline is 16:00 on 2 April 2026.

Other contributions

Easy bank transfer, debit card, Apple Pay, Google Pay

- The deadline for contributions by any of these methods is 23:59 on 5 April 2026. An easy bank transfer (where money goes directly from your bank account to your chosen J.P. Morgan Personal Investing pot) is typically the fastest way to contribute to your ISAs.

Manual bank transfers

- You can manually transfer money from your bank account to your J.P. Morgan Personal Investing account, using your J.P. Morgan Personal Investing account number as a reference. The deadline for most people using manual bank transfers is 16:00 on 2 April 2026.

- If you specifically use CHAPS, the deadline is 16:00 on 2 April 2026. Be aware that depending on your bank, you may need to split your contribution over several days. Additionally, some banks require a manual set-up which may increase the time it takes to process these contributions.

- You’re currently not able to contribute to your LISA by manual bank transfer.

More information on how to pay into your J.P. Morgan Personal Investing accounts can be found here.

Allocation from General Investment Account

- If you have a General Investment Account (GIA), you may want to move money already invested via your GIA into your ISA. This process is sometimes called ‘Bed and ISA’ and involves selling your general investment funds and buying them within an ISA. Any gains on the sale of GIA investments may be subject to CGT. To ensure this is completed within the 2025/26 tax year, this should be requested by 22:00 on 1 April 2026.

Remember, friends and family can also contribute to a J.P. Morgan Personal Investing JISA via manual bank transfers, so it may be a good idea to share the details and deadlines with them if appropriate. You can share the contribution details easily from the mobile app by tapping the “Pay in” button when viewing the JISA.

If you have a pension with J.P. Morgan Personal Investing (indicative dates only)

If you would like to contribute to your J.P. Morgan Personal Investing pension, payments can only be made via Direct Debit at this time. You can't pay into a J.P. Morgan Personal Investing pension by bank transfer.

If you’re making your first Direct Debit contribution into your pension

The deadline is 16:00 on 12 March 2026. The first Direct Debit contribution takes 10 business days to process from when the mandate is put in place. Direct Debits initiated after this date are not guaranteed to reach us before the end of the tax year.

We may also need to ask for documents to verify your identity or support your Direct Debit set-up, in which case, it could take longer to get your contribution set up. So, plan ahead to make sure your pension contributions arrive on time.

If you’ve already set up monthly Direct Debit contributions into your pension

The deadline is 31 March 2026. Any active Direct Debits and active regular contribution expectations set up to collect by the March deadline will be classed as contributions for this tax year and will be reported as such to HMRC. Collections scheduled after this deadline will count towards the next year's tax allowance. The latest date to change an active Direct Debit collection including a one-off increase in contributions is 16:00 on 17 March 2026.

If you need any help

The tax year end can be a busy time, and tax can be complicated. Our mission at J.P. Morgan Personal Investing is to make investing as easy, accessible, and transparent as possible. If you need a helping hand on which investment products could help you to invest tax-efficiently, or would like to speak to someone, our Client Support team is available to answer any of your questions as we approach tax year end. To discuss tax year end in greater detail, please drop us an email at support@personalinvesting.jpmorgan.com or book a free call for more guidance on making the most of your allowances.

Please note that J.P. Morgan Personal Investing cannot give tax advice, so you may wish to speak with a qualified tax adviser about tax allowances.

Risk warning: As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. ISA/JISA/LISA/Pension eligibility rules apply. With LISAs, govt withdrawal charges may apply. Seek financial advice if you're unsure if a pension is right for you. Tax rules vary by individual status and may change. This is general information, not personalised tax advice.