2. Start early and be consistent

We do not recommend trying to ‘time the market’, or constantly trying to identify buying and selling opportunities.

Authors:

Alex Janiaud | Georgina Baker | Euan Jones

Last updated: 21 April 2026

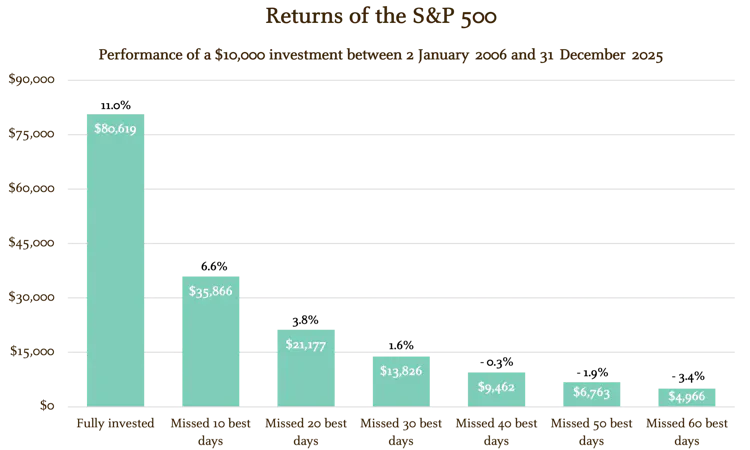

Time in the market, not timing the market

We see little evidence that timing the market works for most investors. While trying to identify the exact right moment to buy and sell sounds appealing, being able to predict events that move markets is almost impossible. We therefore do not believe that timing the market is a useful way to think about investing and achieving your financial objectives and instead advocate ‘time in the markets’.

The chart below illustrates why this matters, especially during periods of market turbulence where it can be tempting to want to take control. Looking at a hypothetical $10,000 investment over the past 20 years, the chart shows how staying invested could have significantly outperformed a strategy of moving in and out of the market during periods of turbulence. While past performance is not a reliable indicator of future performance, in missing some of the market's best days, investors can lose out on opportunities to grow their portfolios, resulting in a potentially harmful impact on overall returns.

Source: J.P. Morgan Asset Management Guide to Retirement using data from Bloomberg.

Returns are based on the S&P 500 Total Return Index, an unmanaged, capitalisation-weighted index that measures the performance of 500 large capitalisation domestic stocks representing all major industries. The hypothetical performance calculations (gross of fees) are shown for illustrative purposes only and are not meant to be representative of actual results while investing over the time periods shown. If fees were included, returns would be lower, and returns will fluctuate. Past performance is not indicative of future returns. An individual cannot invest directly in an index. Data as of 31 December 2025.

Returns after economic and geopolitical shocks:

The below chart shows the performance of a 60/40 portfolio (60% stocks, 40% bonds) against cash, for both one- and three- year timeframes after a series of ‘shocks’ since 1990.

Over the timeframe, the 60/40 portfolio can be seen to have outperformed cash more than 70% of the time, and in all instances over the three-year timeframe. No matter when you invested during this period, a long-term view would have dramatically increased your probability of avoiding losses. Our wealth managers would typically advise against investing with less than a 3-year time-horizon. While past performance can’t guarantee future returns, data consistently backs that longer-term investment perspectives can increase your likelihood of positive outcomes.

Source: Bloomberg, S&P Global, J.P. Morgan Asset Management. 60/40 portfolio is contracted using S&P 500 Index and S&P 10-year US Treasury Note Futures Index. Cash: ICE USD LIBOR (3M). Return calculation begins at the end of the month prior to the shock. Guide to the Markets - UK. Data as of 31 December 2025.

While big market movements can seem significant in the short run, they are more likely to appear as a blip when viewed over several years. Historically, the probability of loss has decreased the longer you hold equities.

Benefits of compound returns

'Compounding', or compound returns, essentially refers to the importance of patience and commitment in investing.

The basic concept is as follows. In the first year of investing, you may generate returns on your initial investment. In the second year, you invest the capital (your initial investment) plus the returns, and you may generate further returns on the total. And so this cycle continues.

The below charts demonstrate the power of investing earlier in life and of compounding, by reinvesting the income from your investments. If you start to save at the age of 25 and invest £5,000 annually in an investment that grows at 5% a year, you'll have nearly £300,000 more by the age of 65 than if you started at 35, even though overall you would only have invested an extra £50,000. As the right-hand chart shows, there is also a significant difference between reinvesting and not reinvesting your income. But don't be discouraged if you're starting a little later. Compounding can reward investors of all ages who choose to start today and not a decade down the road.

Effect of compounding:

Source: (Left) J.P. Morgan Asset Management. For illustrative purposes only. Assumes all income reinvested. Actual investments may incur higher or lower growth rates and charges. (Right) Bloomberg, FTSE, J.P. Morgan Asset Management. Based on FTSE All-Share Index and assumes no charges. Past performance is not a reliable indicator of current and future results. Guide to the Markets - UK. Data as of 31 December 2025.

Of course, investing is subject to the ups and downs of the stock market and there’s a risk you’ll lose some or all of the money you’ve put in, so returns aren’t guaranteed. However, by investing over a long timeframe, you can give your investment time to make up for any losses.

Pound-cost averaging can shield you from market shocks

Investors might consider what is called ‘pound-cost averaging’ – effectively drip-feeding money into their portfolios at regular intervals either by making investing a regular habit, setting a reminder, or an automatic direct debit. This buys you into the markets during the various ups-and-downs, meaning you can be less exposed to short-term market movements.

Our drip-feed feature allows you to maximise your annual tax allowance with a cash pot within an ISA and then invest your money gradually over the months to come, or when is most convenient.

This means that you can enjoy the tax benefits of a stocks and shares ISA while remaining assured your money can be invested slowly but steadily, rather than all at once. You can reduce the risk of buying in just before markets drop and instead stay invested for the market recovery – the speed of which can be very difficult to predict.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio with J.P. Morgan Personal Investing can go down as well as up and you may get back less than you invest. Tax rules vary by individual status and may change. Pension, ISA, JISA and LISA eligibility rules apply. With LISAs, govt withdrawal charges may apply.

J.P. Morgan Personal Investing does not provide tax advice. For personalised advice tailored to your specific situation please consult with a qualified tax adviser or financial planner. If you are unsure if a pension is right for you, please seek financial advice.

J.P. Morgan Personal Investing provides 'restricted advice', which means we will only make investment recommendations on the products and services that we offer.