How much cash do you need?

Alex Janiaud

6 min

Cash and investments should work in harmony, and not in competition with each other. Having a safety net of cash can give you the confidence you need to invest, knowing that the value of your investments could fall. We explore some principles for deciding how much to allocate towards cash.

At a glance

- It’s sensible to have cash reserves that can help you meet living expenses and emergencies

- At the same time, keeping too much of your money in cash leaves your savings vulnerable to inflation, and also leaves you at risk of missing out on the growth potential of investing it in financial markets

- Understanding how much cash you need depends on a few factors, including your time horizon and your financial objectives

Everyone needs cash. Living expenses need to be paid for, and we all need to be ready for an unexpected drain on our finances, such as a medical emergency or a loss of employment.

Investing can be an effective way of ensuring that we have enough money to meet our most important needs. We are staunch advocates of people putting their savings to work. Keeping too much of your money in cash leaves it vulnerable to being eroded by inflation, while you may also miss out on gains that can be made through investing in financial markets (although be mindful that you could also lose your money through investing). Investing is typically a great way to help you build towards your financial objectives, such as helping children to get onto the property ladder.

That said, tying up too much of your money in investments could leave you with little room to manoeuvre should you suddenly need to support yourself or a loved one in a way that stretches beyond your normal income.

Cash and investments should work in harmony, and not in competition with each other. Having a safety net of cash can give you the confidence you need to invest, knowing that the value of your investments could fall.

Finding the right balance can be tricky. J.P. Morgan Personal Investing wealth experts are on hand to help clients set their balance between cash and investments. It’s often a good idea to seek advice when drawing up a plan for your finances, but there are some factors that you can consider yourself when calculating how much cash you need.

Calculating your cash buffer

It’s helpful to build a hierarchy of spending needs when it comes to figuring out how much cash you should have.

- You should have a rainy-day fund for potential financial emergencies, as you don't want to have to sell your investments at the wrong time in order to stay financially afloat during these periods. Your personal circumstances will dictate the amount of emergency cash that you need. We would usually suggest between three and six months’ essential spending.

- Once you’ve established this buffer, it’s worth estimating how much cash you need to support your living expenditure, and how it compares with your income. If you are planning any large outlays in the next two years, such as on a house or a car, we think it’s a good idea to keep that money in cash, rather than invest it. You can use the Money & Pension Service’s budget planning tool to help measure your income and spending.

- It pays to think about saving for your latter years too, particularly as retirement draws closer. If you're retiring in the next few years, work out what your annual expenditure may be, along with any capital expenditure, and consider having cash available for this period.

As a guide, the Pensions UK trade body estimates that a one-person household will need to spend £43,900 annually to enjoy a comfortable retirement – one that includes financial freedom and some luxuries. This threshold rises to £60,600 per year for a two-person household. It is likely that you will have some retirement income in the form of a workplace pension, as well as the state pension, but it can be a good idea to put cash aside to supplement this money.

The death of a spouse might reduce pension income from workplace pensions or state pensions. J.P. Morgan Personal Investing wealth experts stress test this scenario for their clients, and it’s worth considering when trying to forecast how much money you’ll need towards the end of your life.

Put your money to work

Cash has a role in your portfolio. But it shouldn’t become the whole portfolio.

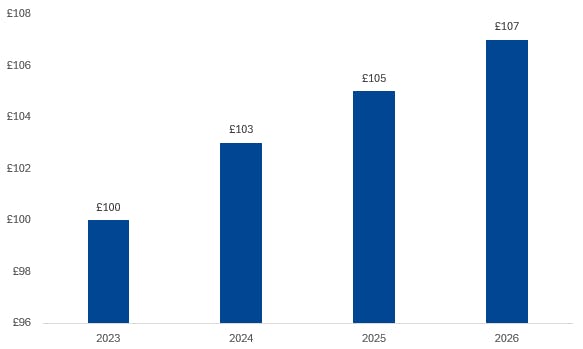

Sitting on too much cash lowers our purchasing power. The below chart shows how the value of the pound is forecast to decline from 2023 to 2026. By 2026, £107 is predicted to have the same purchasing power as £100 in 2023.

Source: J.P. Morgan Wealth Management, Bloomberg Financial L.P. Uses Fed Core Personal Consumption Expenditures inflation forecasts, ECB Harmonised Index of Consumer Prices forecasts, and BoE Consumer Price Index inflation forecasts. Data as of 31 January 2024

An uncertain world and higher savings rates might encourage people to keep their money in cash, instead of investing. Loss aversion, which pushes people to avoid loss instead of seeking gain, is a very powerful force in behavioural finance. Taking an overly prudent approach can, however, cost you money and make it harder to meet your financial objectives. Depending on how much you earn, you may have to pay tax on savings interest, including interest accrued in your bank account.

“Cash feels safe because the number stays the same,” says Jeff Kreisler, Head of Behavioral Science at J.P. Morgan Private Bank. “But that number doesn’t represent the power of money that – in cash – is shrinking every day.”

“It’s what we can do with money that matters, and what we can do is not always safe,” he continues.

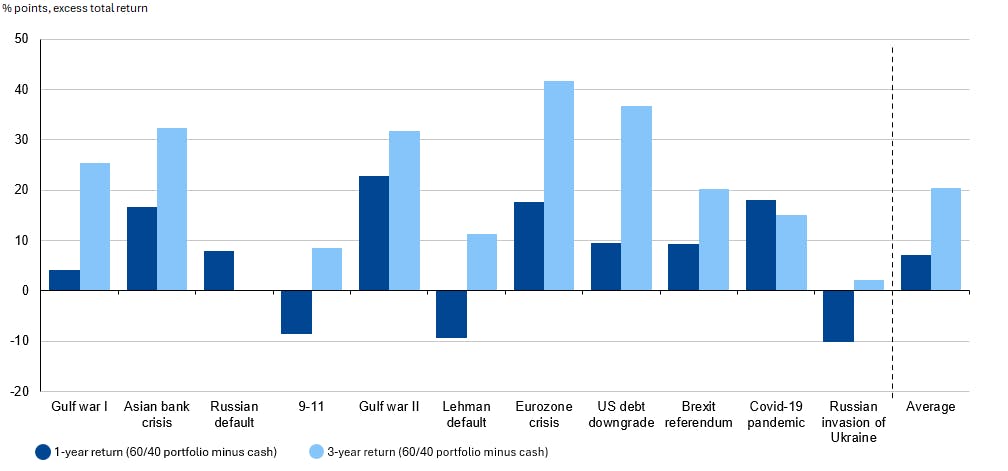

Consider too, the relative returns of cash and investments. Recent history indicates that cash is unlikely to outperform a multi-asset portfolio. J.P. Morgan Asset Management analysis of the periods following a selection of geopolitical and economic shocks since 1990 shows that a portfolio composed of 60% equities and 40% government bonds has outperformed cash more than 70% of the time over a one-year horizon, and always outperformed over the three-year timeframes. Therefore, hiding in cash has historically been an incorrect approach.

Source: Bloomberg, S&P Global, J.P. Morgan Asset Management. '0’ represents holding money in cash. 60/40 portfolio is constructed using S&P 500 Index and S&P 10-year US Treasury Note Futures Index. Cash: ICE USD LIBOR (3M). Return calculation begins at the end of the month prior to the shock. Data as of 30 November 2025. Past performance isn't a reliable indicator of future performance.

It’s a good idea to tailor your investments in accordance with your time horizon. As you progress towards the end of your career, you may wish to adopt a medium level of risk to build for the midpoint of your retirement, with higher risk investments for your latter stages, when these investments will have had longer to potentially withstand the higher volatility associated with investments that carry more risk. This process, by which we apportion different risk levels to parts of our savings, is known as cashflow bucketing.

Get advice

Ensuring that your cash and your investments work together isn’t always straightforward. Through our paid advice offering, a J.P. Morgan Personal Investing wealth expert can help you identify your pyramid of financial needs and set the right equilibrium between cash and investments. Our free guidance offering, meanwhile, can also offer a forum for discussing how much cash you need.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. Seek financial advice if you're unsure if a pension is right for you. Tax rules vary by individual status and may change. This is general information, not personalised tax advice. Past performance and forecasts are not a reliable indicator of future performance. We provide 'restricted advice', meaning we only make investment recommendations on the products and services that we offer.