US equities have outperformed most other markets over the past decade, driven by superior corporate earnings growth. This consistent performance has led to higher valuations, and while the market is expensive compared to historical averages, we expect 2026 to be another strong year.

The main drivers are:

- The ongoing artificial intelligence (AI) revolution in the US, and

- Supportive government policies.

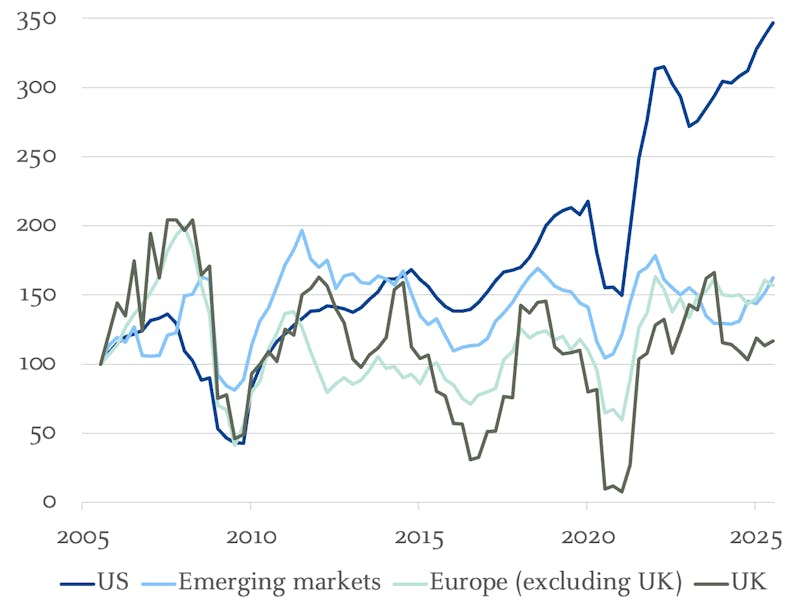

Chart 1: US companies' earnings per share (EPS) growth over the last 20 years stands out

Notes: Data rebased to 100 from July 2005. Data from July 2005 to July 2025.

Source: Macrobond, J.P. Morgan Personal Investing. Past performance is not a reliable indicator of future performance.

Despite political debate around tariffs in 2025, President Trump’s One Big Beautiful Bill (OBBB) – the US president’s flagship tax and spending bill – is providing notable stimulus in two key areas:

- Firstly, a tax rebate for consumers will strengthen already healthy household balance sheets.

- Secondly, and perhaps more importantly for the equity markets, the favourable tax treatment of capital expenditure (capex) encourages businesses to accelerate investment projects.

Substantial capex is expected from the AI ‘hyperscalers’ – those companies providing the cloud services infrastructure necessary for the functioning of AI. This encompasses some of the ‘Magnificent 7’ US tech companies, seven of the largest and most influential companies in the world. These are: Apple, Amazon, Alphabet (Google’s parent company), Nvidia, Microsoft, Meta and Tesla.

However, through productivity and efficiency gains, the benefits are likely to extend across other companies in the S&P 500 index, which reflects the performance of the 500 largest publicly traded companies in the US.

Future spending concerns?

There are reasonable concerns about spending beyond 2026 and the cash flow required to sustain it. If these issues are not addressed, the ‘AI bubble’ narrative may become more prominent.

Chart 2 below shows the earnings growth expectations for the group of Magnificent 7 tech stocks, compared to the other 493 members of the S&P 500. Expectations for the Magnificent 7, which have been incredibly high, have begun to fall more in line with the other index constituents for the coming years.

Chart 2: Earnings growth expectations, year on year (%)

Notes: Bloomberg Magnificent 7 Index, 493 = Bloomberg 500 ex Magnificent 7. Growth rates: year on year of full calendar year earnings per share (EPS). 2025 onwards, shown in grey, are Bloomberg Estimates of the EPS in that calendar year, reflecting a composite of expectations from sell side analysts and strategists. Data accurate as at 28 November 2025.

Source: Bloomberg, Macrobond, J.P. Morgan Personal Investing

A tailwind from the Federal Reserve

Another positive for the US economy and equity market is the Federal Reserve’s ‘easing’ cycle. In December 2025, the Federal Reserve ended its quantitative tightening programme, which had been reducing the balance sheet built up during the Global Financial Crisis and the COVID-19 pandemic, effectively withdrawing money from the financial system. In addition to stopping this withdrawal, the Federal Reserve has also lowered the Fed Funds rate, similar to the Bank of England’s Cash Rate, reducing the cost of new borrowing and stimulating economic activity.

Our outlook for the US economy and equity market is a positive one but we are cognizant of current valuations.

As shown in chart 3, the 1-year forward price-to-earnings (P/E) ratio has reached similar peaks as seen during the pandemic and dotcom eras. We are not put off by this for 2026. Valuations have very limited predictive power for short-term performance.

The denominator – earnings – has shown to be stronger over the past decade, before the evolution of AI.

Chart 3: The S&P 500’s 1-year forward P/E Ratio

Notes: P/E ratio compares a company’s share price to earnings per share, indicating how much investors are willing to pay for each dollar of earnings. Data accurate as at 28 November 2025.

Source: Macrobond, J.P. Morgan Personal Investing.

In summary

In 2026, we expect US equities to benefit from continued AI adoption, with the broader market likely to catch up as the advantages of AI spread and the overall strength of the US economy persists.

About this update: This video was filmed on 8 December 2025.

Source for Outlook data: MacroBond, J.P. Morgan Personal Investing and Bloomberg.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down as well as up and you may get back less than you invest. Past performance and forecasts are not a reliable indicator of future performance. We do not provide investment advice in this update. Always do your own research.