How should investors react to geopolitical uncertainty in the Middle East?

Alex Janiaud

4 min

When dealing with geopolitical uncertainty it’s helpful to focus on what we know and stick to long-term investing principles. Recent events in the Middle East are no exception.

In light of recent geopolitical conflicts involving the US, Israel, Iran and other gulf nations, UK investors may be concerned about the potential impact on their portfolios in the short and long term.

With the situation moving quickly, we must look at what we know and not speculate where we cannot.

While markets have experienced volatility throughout this conflict, our long-term 2026 Investment Outlook has remained consistent.

What we know

Volatility has returned to financial markets after a period of calm. Geopolitical flashpoints are common and often a source of volatility spikes. For example, we witnessed a modest spike in response to strikes by the US on Iranian infrastructure in June last year, and a bigger spike after the roll-out of tariffs by the US in April 2025.

Volatility is a natural part of the investing journey, so we encourage investors to take a long-term view of financial markets rather than reacting to external events which might have a much shorter, albeit unpredictable, duration.

“Recent tensions around energy infrastructure appear largely tit-for-tat, with both sides using or being encouraged by third parties to talk,” says Scott Gardner, Investment Strategist at J.P. Morgan Personal Investing.

On 21 March, the US President issued a deadline to Iran calling for an end to attacks on ships crossing the Strait of Hormuz within 48 hours. On 23 March, the President then announced that the US and Iran had opened a dialogue and that US attacks on Iranian energy infrastructure had been postponed for five days. An Iranian news agency has, however, quoted an unnamed source from Iran's foreign ministry who has denied that any direct talks between the US and Iran have taken place.

“While sustained attacks on infrastructure would be disruptive to markets, these are fast‑moving events and it’s important to try to avoid pre-empting what might happen next,” Gardner continues.

“We’ve already rebalanced to take advantage of the decline in equities and, while we aren’t currently making significant changes in response to the conflict, we stand ready to act should opportunities arise. We encourage clients to retain a long-term perspective.”

What can investors do?

As an investor, trying to remain focused on the long term during crises can be difficult. However, our analysis shows that over the long term, investors in a wide variety of equity and bond markets outperform cash savers. It should be noted that while historic data can be a useful reference point, when investing nothing is guaranteed and capital is at risk. Past performance is not a reliable indicator of future performance.

Although none of us can control the news, or the reactions of other investors around you, you can control the impulse to make hasty decisions. Many of our seasoned investors already know this, because in the past the vast majority of our investors have ridden out these market storms without changing their portfolios*. However, if you’re feeling nervous about how recent financial market performance could affect your investment goals, our team is here to talk.

The investment team continues to actively manage portfolios for its Fully Managed, Socially Responsible Investing and Thematic Investing clients. The Smart Alpha portfolios are actively monitored by the J.P. Morgan Asset Management team who provide guidance to our investment team on changes to portfolios based on market conditions, leveraging their deep research-driven insights. For Fixed Allocation clients, portfolios are adapted once a year. Long-term investing can reward attention to economic and business fundamentals, which are more long-lasting than geopolitical events.

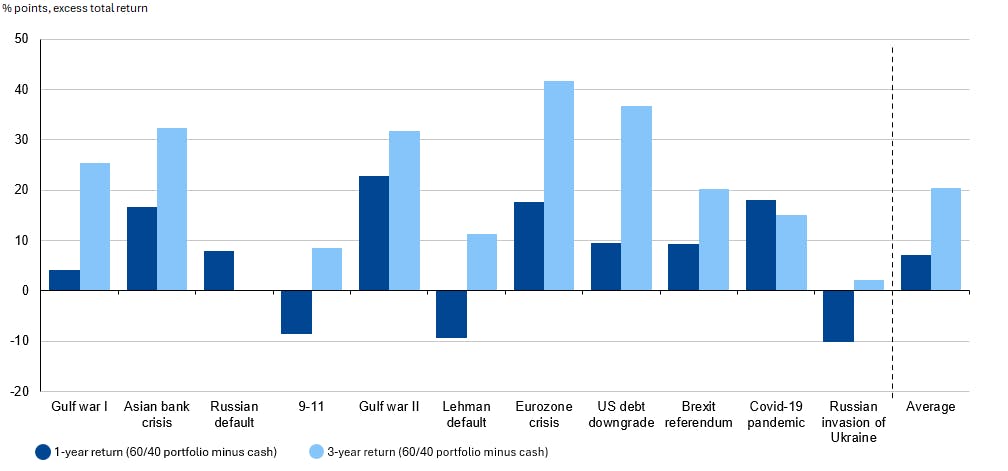

During a tumultuous period it might be tempting to withdraw some investments and remain in cash. It’s worth considering, however, the relative returns of cash and investments. Recent history indicates that cash is unlikely to outperform a multi-asset portfolio. J.P. Morgan Asset Management analysis of the periods following a selection of geopolitical and economic shocks since 1990 shows that a portfolio composed of 60% equities and 40% government bonds has outperformed cash more than 70% of the time over a one-year horizon, and always outperformed over the three-year timeframes. Therefore, hiding in cash has historically been an incorrect approach.

Hiding in cash is typically not the way to avoid geopolitical risk

Subsequent 1-year and 3-year returns over cash, following market shocks

Source: Bloomberg, S&P Global, J.P. Morgan Asset Management. '0’ represents holding money in cash. 60/40 portfolio is constructed using S&P 500 Index and S&P 10-year US Treasury Note Futures Index. Cash: ICE USD LIBOR (3M). Return calculation begins at the end of the month prior to the shock. Data as of 30 November 2025. Past performance isn't a reliable indicator of future performance.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio with J.P. Morgan Personal Investing can go down as well as up and you may get back less than you invest. Past performance and forecasts are not reliable indicators of future performance. Thematic investing carries specific risks and is not for everyone. We do not provide investment advice in this article. Always do your own research.

*In 2022, we looked at seven events going back to 2012 to see if our clients changed their behaviour in response to market volatility. An average of 97.8% of our clients did nothing out of the ordinary.