Our approach to ETFs

Why ETFs are our investment vehicle of choice

Cost efficiency

An ETF tracking a developed equity market such as the S&P 500 can cost as little as 0.05% of the capital you invest in the ETF per year. At times, the cost of investing in active ETFs can be slightly higher, however, this comes with the potential for outperformance, or the potential to achieve a specific investment outcome, such as a certain level of income generation. They offer a cost-efficient way to target investment outcomes that may not be possible by solely using passive ETFs.

Diversification

Investing in ETFs is an effective way to create a globally diversified, multi-asset portfolio. Passive ETFs can be used as core building blocks of a portfolio, such as those following broad-based and well diversified indices, spreading the risk of your investments across many securities. Buying an ETF that tracks an index such as the S&P 500, which would typically use the ‘full replication’ method, is comparable to buying a small part, in the appropriate proportion, of each of the 500 largest US-based companies. This is more straightforward than it would be for an individual to do themselves, as well as coming at a much lower cost.

ETFs like these can be the building blocks of a portfolio that can then be complemented by ETFs that provide exposure to more specific asset classes. This may be regional or sectoral ETFs for example, as well as active ETFs that aim to outperform their reference index or achieve specific investment objectives.

Our investment team constructs portfolios using a mixture of ETFs covering different asset classes, enhancing the diversification of portfolios.

Choice

Our investment team chooses from a universe of around 2,000 ETFs. We consider many factors in choosing our investments and hold both physically-backed and synthetic ETFs with high liquidity, so that they are easier to buy and sell. The investments in our portfolios are reviewed regularly to ensure they're the most suitable for our customers' needs.

Flexibility and liquidity

Just like individual stocks, ETFs can be traded whenever the relevant stock exchange is open, making them a flexible way to invest. This is unlike some other collective investment vehicles like unit trusts, which typically trade at one set price point during the day. They have also proved to be an effective vehicle for fractional trading – where partial shares of ETFs can be traded rather than whole units – as we do at J.P. Morgan Personal Investing. This has opened up investing to a wider audience.

Transparency

Investors are typically able to see the underlying positions the ETF is invested in on a daily basis. This is not the case across all other types of collective investment vehicles.

How we select our ETFs

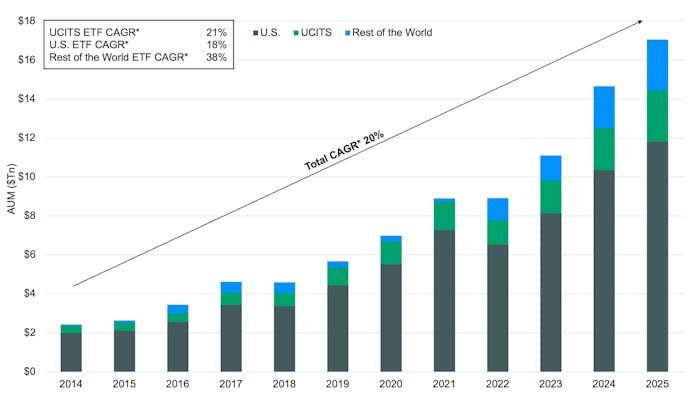

The ETF market has grown substantially in recent years: assets under management have increased from a little over $2 trillion in 2014 to stand at more than $17 trillion in July 2025. There are now around 12,400 ETFs available worldwide*.

Global ETF AUM growth over time

Source: J.P. Morgan Asset Management’s Guide to ETFs, data as at 31 July 2025. CAGR stands for compound annual growth rate and reflects the rate at which the global ETF assets under management (AUM) would have grown by between 2014 and 2025 if it had been at a consistent rate, compounded annually.

Being able to choose the right funds is as important as ever but has become increasingly complex. Having a deep level of knowledge of the market and extensive experience in selecting ETFs puts us in a position to make highly informed selection decisions for our managed portfolios.

For these portfolios, for each asset class, region or market segment, we find what we consider to be the best ETF, while continuously monitoring alternatives. As our aim is to provide a diverse set of opportunities for our clients, we assess as many ETFs as possible. Once the funds are chosen, we then use our expertise to blend them together so that our managed portfolios can benefit from a rich diversity of investment exposure while staying within their risk levels.

Key considerations when assessing which funds to include in portfolios:

The components of the market index

As outlined earlier, many passive ETFs aim to track and replicate the performance of a particular index, like the FTSE 100. Indices follow rules-based methodologies and for a large, liquid index like the FTSE 100, ETFs would typically be ‘physical’ and employ full replication. Essentially, they are constructed by ‘weighting’ each underlying company in the FTSE 100 according to its market capitalisation (size) as a share of the index. For other indices, there can be specific factors that result in there being a large weight in one particular company, sector or country.

By looking at the underlying components – in the case of the FTSE 100, the companies – we can judge whether an index is, in our opinion, a suitable investment and whether it accurately reflects our investment team’s view.

Method of replication and tracking error

The method for holding the physical components of an index varies from fund to fund, and is dependent on the characteristics of the market and the fund’s investment objectives. Many ETFs use a system of optimisation, where a sample of the holdings is used to replicate the index’s performance as a whole, using quantitative methods.

In order to do this, we look at what is known as the tracking difference of each ETF – how closely the ETF manager has matched the performance of the index – and look to select funds which are as closely aligned as possible.

Costs

Subject to other factors listed here, we aim to hold the fund with the lowest overall cost in each asset class. The main costs associated with this are:

- The ETF’s total expense ratio (TER) – a measure of the annual cost to the investor of holding the ETF

- The ETF’s internal trading cost, which reflects how much trading impacts fund performance.

We seek to select the fund that delivers the most overall value for our clients.

Size and trading volume

How much money is invested in an ETF, its trading volume and subsequently its liquidity, tend to be closely related. We avoid investing large amounts in ETFs where trading volume is limited, as it can be more difficult and costly to trade. This is typically a function of the ETF’s underlying market, as some holdings are more liquid and easier to trade than others.

We aim to use the ETFs with the lowest bid-offer spreads – the smallest gap between the cost of buying and selling each fund. While a low TER may look attractive, if the bid-offer spread is very large and/or the fund size is very small, we would not necessarily use that fund until these conditions have improved, as it could make trading more expensive and/or more difficult. We also seek to understand the liquidity dynamics for the underlying index holdings, as this can be an important factor.

The type of ETF

There are two main types of ETFs: “physical” and “synthetic”. We predominantly invest in physical ETFs, whilst also allocating to synthetic ETFs where the balance between risk and reward is particularly attractive. This is especially the case for large US equity indices where dividends would be subject to 30% withholding tax (for funds domiciled in Luxembourg) and 15% (for Irish-domiciled funds). This is something that could impact ETFs operated on a physical basis, as they hold the underlying components of the index and therefore receive dividends in the event these are paid by the constituent companies. This can make synthetic ETFs more attractive for some markets, as this tax-related factor may not impact them.

Once we’ve selected our ETFs, we use proprietary macroeconomic and market research to assess the asset allocation of our portfolios and rebalance or make changes when opportunities arise.

* J.P. Morgan Asset Management’s Guide to ETFs, data as at 31 July 2025.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. Tax rules vary by individual status and may change.