J.P. Morgan Asset Management: What forces will shape markets over the next decade?

Andrew Lacey

6 min

Lead portfolio managers, researchers and strategists at J.P. Morgan Asset Management believe that investors face a rapidly changing world. Diversification, flexibility and a willingness to embrace the new will be crucial to portfolio resilience.

This article is aimed at experienced investors owing to its technical nature.

J.P. Morgan Asset Management publishes an annual ‘Long-Term Capital Market Assumptions’ (LTCMA) report – to which J.P. Morgan Personal Investing also contributes – which explores the firm’s long-term expectations for financial markets and the forces that shape them. At the core of the research sits a 10-to 15-year outlook for risks and returns across asset classes.

The firm has recently published its 30th edition of the LTCMA report, and we have summarised its highlights below.

The Big Picture: Change and Adaptation

Over the past three decades, markets have weathered the internet revolution, the dot-com bubble, the rise of China, the global financial crisis, quantitative easing, the pandemic, and the dawn of artificial intelligence (AI).

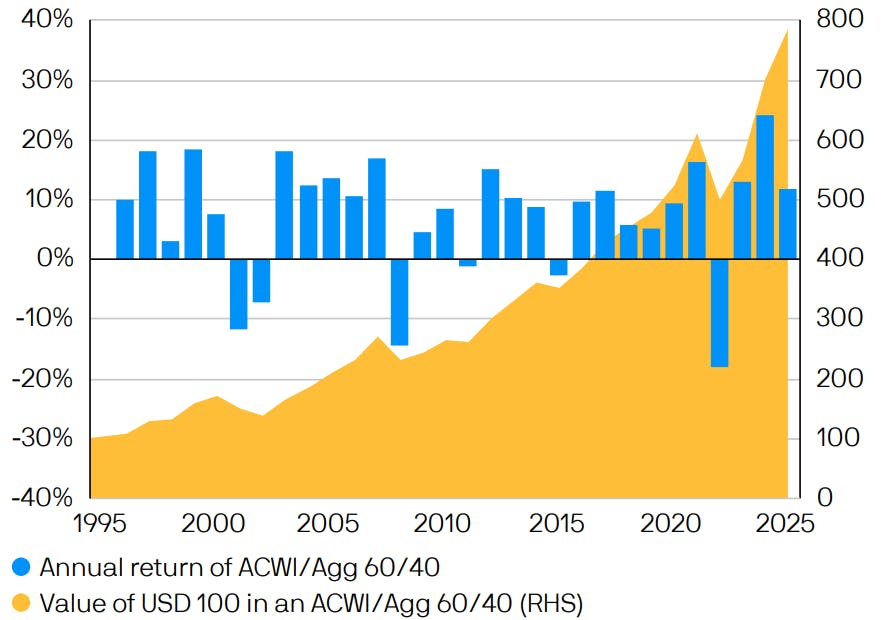

Despite these challenges, global bonds have delivered annualised returns of 4.3%, and global stocks 8.3%. A £100 investment in a classic global 60/40 portfolio in 1995 would be worth £667 today (MSCI ACWI / U.S. Aggregate Bonds).

This resilience is a reminder: economies and markets adapt.

A steady exposure to stocks and bonds has stood the test of time over three decades

Growth of a 60/40 equity to bond portfolio allocation, over 30 years, and average returns through the period

Source: Bloomberg, J.P. Morgan Asset Management; data as of September 30, 2025. Past performance is not a reliable indicator of future performance.

Today, the world faces new headwinds, but also new tailwinds. In particular, the LTCMA report examines how rising economic nationalism and fiscal activism are reshaping the investment landscape, which may create both challenges and opportunities for investors. Understanding these two concepts is fundamental to many of the insights below.

Economic nationalism relates to the adoption of economic policies that may, among other things:

- Prioritise domestic growth

- Protect domestic industries

- Reduce the dependency upon foreign production or investment.

Fiscal activism relates to the willingness of governments to use fiscal tools such as taxes and investment spending to stimulate the economy. Fiscal policy is a common element of a government’s broader approach to managing a country’s economy, usually in balance with monetary policy (adjusting how much money is in the economy, and the cost of borrowing). However, fiscal activism suggests that government spending is playing, or set to play, an increasingly prominent role in pursuing economic objectives.

Economic Nationalism: A Double-Edged Sword

The trend toward economic nationalism, especially in the US, is reshaping global economic growth. Trade frictions can squeeze productivity and with tighter immigration controls reduce the availability of labour. Many countries, facing aging populations and declining birth rates, are struggling to maintain growth.

That said, the LTCMA report suggests these challenges are also spurring positive change. Export-driven economies such as Germany and Japan are now investing more at home, stimulating domestic demand. China may follow suit. Meanwhile, companies are turning to technology to offset labour shortages, accelerating the adoption of AI and other innovations.

The result? Global growth is forecast to hold steady at 2.5%, with the US growth advantage expected to narrow but not disappear. While economic nationalism can be disruptive, it also forces regions to innovate and invest, potentially redistributing growth more evenly across the globe.

Fiscal Activism: Governments Step Up

Fiscal activism – governments using spending and taxation to drive growth – has moved to centre stage. The pandemic ended a decade of austerity, and 2025 saw a surge in government spending, especially in Europe. Germany, for example, has loosened its “debt brake” to fund domestic demand and defence – a historic shift.

As governments increase their spending commitments, corporations are expected to follow suit with a new wave of capital investment (capex).

Large firms hold trillions in cash ready to deploy. A pickup in fiscal spending and capex supports both the LTCMA growth forecasts and projections for company profits.

In the US, fiscal spending remains high, though new tax cuts are more about shifting capital than boosting growth. In Europe, increased government spending is narrowing the growth gap with the US.

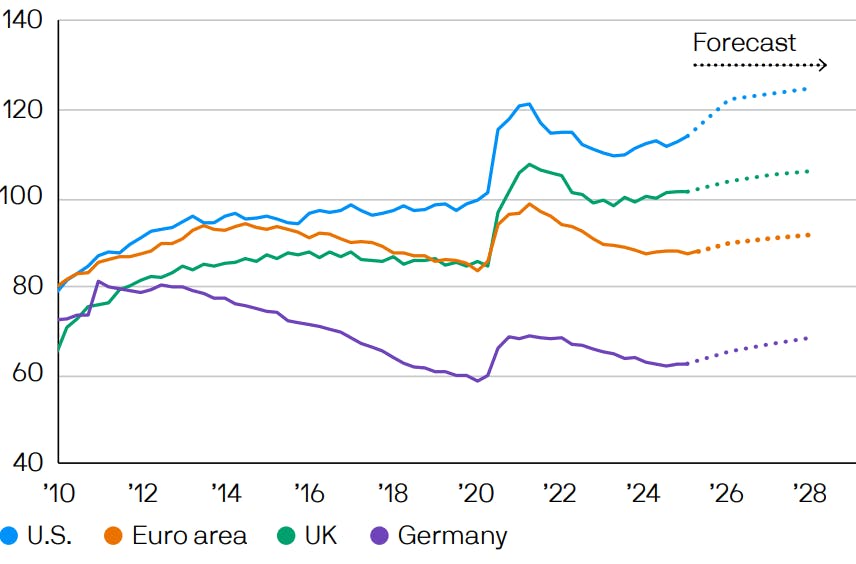

Fiscal commitments push up debt-to-GDP across the globe

Debt-to-GDP trajectories of major economies, given fiscal commitments

Debt-to-GDP ratio

Source: Bank for International Settlements, Eurostat, IMF, LSEG Datastream, J.P. Morgan Asset Management; data as of August 31, 2025. Debt refers to gross debt at face value. Dotted lines represent IMF forecasts.

However, higher spending brings risks: rising debt and deficits, and concerns about sustainability. The pressures may push bond yields higher, meaning borrowing for governments will become more expensive, while the value of currencies may be impacted.

Inflation, Bonds, and Currency

Inflation is expected to move up and down a lot (inflation ‘volatility’) over the next decade. Increased inflation volatility and higher starting yields mean holding intermediate term government bonds like US Treasuries is more attractive now than it has been for a long time. That said, greater volatility in inflation means investors could consider an allocation to ‘alternatives’ to improve risk-adjusted performance. Alternatives is a broad category, referring to investments that behave differently to traditional asset classes such as bonds and equities. Examples of alternatives could include exposure to real estate or commodities, amongst a wide array of other options.

The LTCMA report forecasts that the US dollar, which has weakened, could decline further. This suggests investors could assess their exposure to the US dollar, and consider diversifying their currency exposures if appropriate.

Technology: The Race from Adoption to Deployment

Technology adoption, especially AI, is an incredibly strong force driving corporate investment. Governments are incentivising investment in its development, but the real driver is competitive pressure – firms must innovate or risk being left behind.

The US remains the global leader in technology, with the LTCMA report suggesting it will remain so over the coming decade. China, for example, is investing heavily in AI development as well, but the US' ability to restrict Chinese access to important components could impede its development of the technology.

More broadly though, as AI moves from adoption to widespread deployment, the benefits are expected to spread beyond tech giants and into other sectors.

Former IBM chief executive officer Ginni Rometty captured the sentiment: “Artificial Intelligence will not replace humans, but those who use AI will replace those who don’t.”

Put simply: If a firm is not at the cutting edge of deploying AI, somebody else’s is.

Portfolio Resilience in a Shifting World

Technology deployment is a source of optimism, but also a potential destabiliser. Productivity gains are essential as labour force growth slows, but they risk leaving parts of society behind, potentially fueling polarisation and further economic nationalism.

The next decade will be marked by significant change across sectors, geographies, and companies. Historically, such periods favour those who allocate capital actively and globally, across a wide range of assets.

To manage risk appropriately, portfolios should be constructed in such a way that they can withstand inflation, interest rate shocks, and economic volatility. Diversification will remain central to robustness and resilience.

Silver Linings Amid Uncertainty

While protectionism and isolationism pose economic risks, the scale of investment from governments and companies at play is a powerful offset. US leadership in technology and research & development should be supportive of US equities, even as trade policy weighs on the dollar.

For investors, the message is clear: diversify globally, embrace alternatives, and focus on resilience. The shifting landscape offers challenges, but also silver linings for those prepared to adapt.

The world is changing, but markets and economies have always found ways to adapt. Investors who stay flexible, diversify, and embrace new opportunities will be best placed to capture opportunities that emerge.

This summary is based on the 2026 Long-Term Capital Market Assumptions, J.P. Morgan Asset Management.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. Past performance and forecasts are not a reliable indicator of future performance. We do not provide investment advice in this article. Always do your own research.