Should you open a Stocks and Shares JISA?

Alex Janiaud

10 min

A Stocks and Shares Junior ISA (JISA) can be a highly effective way to invest on behalf of a child. As it sits outside of your normal ISA allowance, it can be worth considering opening a Stocks and Shares JISA ahead of tax year end.

At a glance

- A Stocks and Shares JISA can help you invest on behalf of a child so that they may fund substantial outlays, such as for higher education or a home deposit

- They can also serve as useful tools for parents to pass down their wealth

- Parents will never have control over how this wealth is used, so it’s a good idea to provide some financial education to your child before they can access this money. This article offers some tips for teaching your child about money and explains how our wealth experts can help.

A Stocks and Shares JISA lets you invest for your child until they're 18, while protecting any returns from UK Income and Capital Gains Tax up to the annual limit. You can invest up to £9,000 each tax year in a JISA, per child. Crucially, this figure does not form part of your standard annual ISA allowance of £20,000.

Children cannot access their Stocks and Shares JISA until the age of 18. At this point, it will convert into a Stocks and Shares ISA and be under their control. This can be a source of concern for some parents, which we’ll address later in this article.

Parents can also open a Cash JISA for a child, which is a tax-efficient savings account for children under 18, although we do not offer Cash JISAs. A child can have one Cash JISA and one Stocks and Shares JISA, but no more. If you have multiple children, you can open a Cash ISA and a Stocks and Shares ISA for each of them. You cannot have a JISA if you already have a Child Trust Fund for your child. You will need to transfer the Child Trust Fund to a JISA provider and it will be automatically converted.

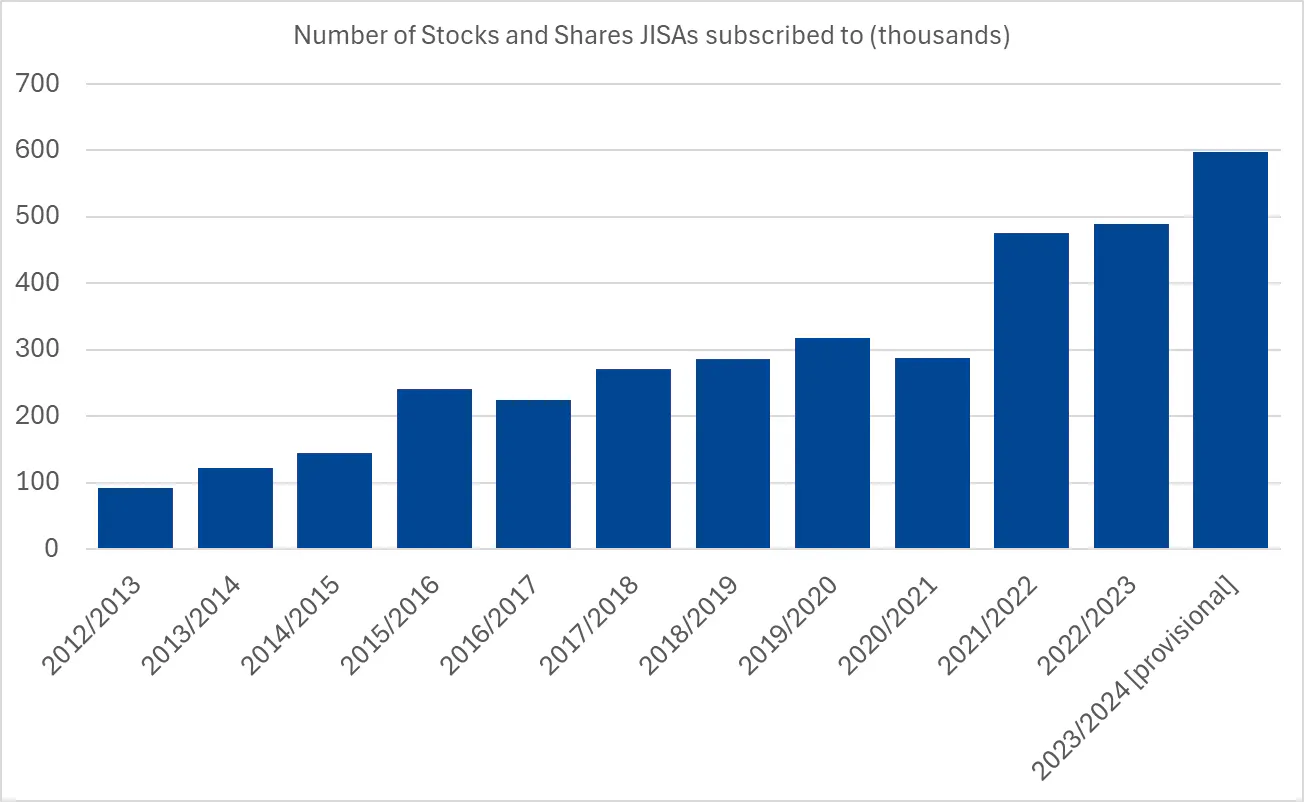

The number of Stocks and Shares JISAs being subscribed to has steadily increased since their inception in late 2011, and has boomed since the coronavirus pandemic. The average amount saved into a Stocks and Shares JISA in the 2024/25 tax year was £3,391, per the Investment Association trade body.

Annual subscriptions to Stocks and Shares JISAs have more than doubled since the 2020/2021 tax year

Source: HMRC Individual Savings Account Statistics, September 2025

The weeks leading up to the end of the tax year on 5 April can be a good moment to open a Stocks and Shares JISA, particularly if you have used up your own ISA allowance. The new tax year, which kicks off on 6 April, is also a good time to reset and plan how best to maximise the allowances afforded by tax wrappers such as the Stocks and Shares JISA. Parents or guardians can open a child’s Stocks and Shares JISA with J.P. Morgan Personal Investing before the child turns 16, which anyone can contribute towards. You can also transfer a Stocks and Shares JISA from another provider to J.P. Morgan Personal Investing.

Three advantages of the Stocks and Shares JISA

Compound returns

Investing in a Stocks and Shares JISA over a sustained period can produce a sizeable pot for your child.

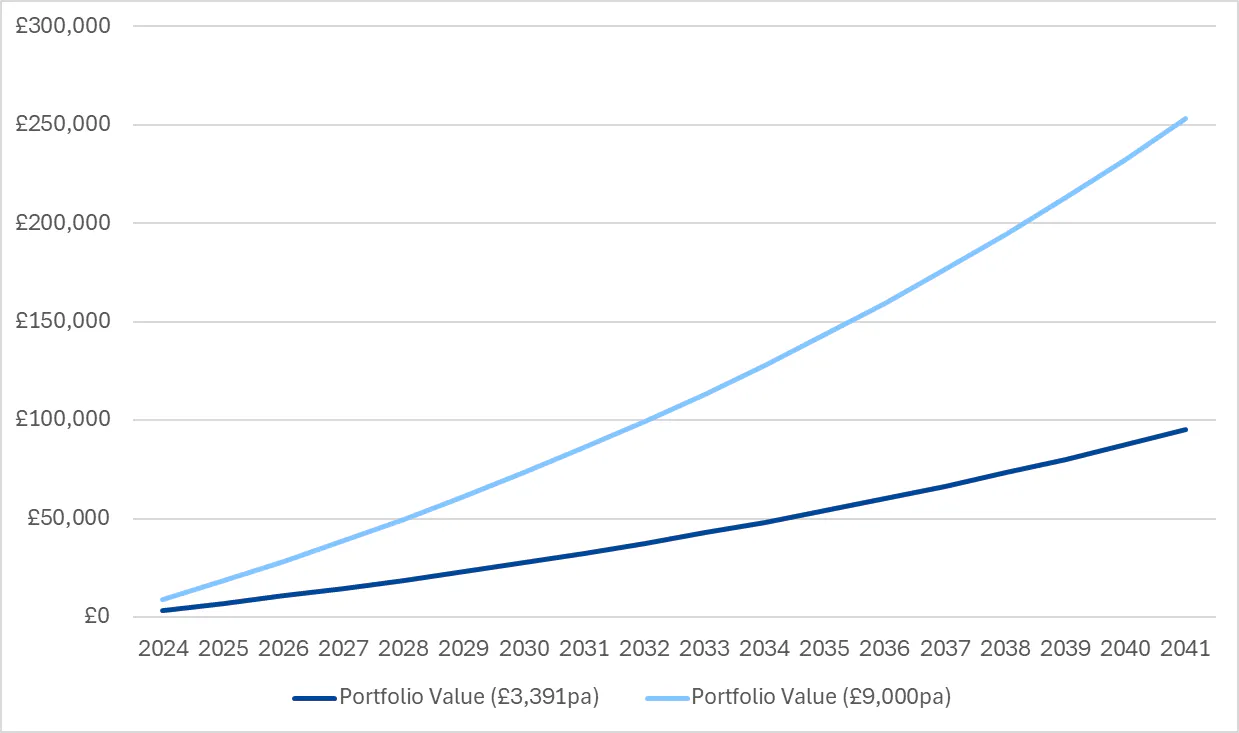

The below chart demonstrates the power of investing over the long term and compounding returns. Compounding occurs when you keep any returns invested to earn more on your new, higher balance. In other words, you can make money on money you've already made.

The chart is an example of how much a Stocks and Shares JISA could have grown if in 2024 you had invested £3,391 per year – the average amount invested in the 2024/25 tax year¹ – on behalf of a child born that year until they reach 18. It compares this with contributions of £9,000 per year, the maximum amount, over the same timeline. The chart assumes an average rate of return of 5%.

Source: J.P. Morgan Personal Investing. The information is not a replacement for professional advice or original research. For personalised advice tailored to your specific situation please consult with a qualified financial adviser. Always do you own research. Forecasts were calculated applying an annual rate of return of 5% to annual contributions of £3,391 and £9,000. Data is illustrative and does not represent actual or future performance. This data does not take into account the effects of inflation or costs and charges. You can make your own forecasts using our Compound interest calculator.

“Even if you don’t use the full JISA allowance every tax year, contributing towards a JISA every month can be a very good way of having an organised approach to accumulating wealth for a child,” says Claire Exley, Head of Financial Advice and Guidance.

A survey conducted by the Investment Association found that education (49%) and helping their child get onto the property ladder (38%) were the primary motivations for parents paying into a Stocks and Shares JISA.

“Accumulating wealth via a JISA can help your child to pay for higher education without having to take out a loan, which could incur heavy interest payments once they’ve graduated from university,” Exley said.

Pass down wealth

Contributing towards a Stocks and Shares JISA can also be a useful way of passing wealth down to your child.

The number of estates liable for Inheritance Tax (IHT) has been on the rise, lifting to 31,500 estates in the 2022/23 tax year – a 13% increase on the prior tax year. The government plans to include most unused pension pots and death benefits within IHT calculations from 6 April 2027, while the IHT nil-rate bands will be frozen until 2031, bringing more estates into scope due to potential rising property and asset values. Were you to gift a sum to your children to pay for a large outgoing, this could also incur IHT. It’s worth bearing in mind that contributions towards a Stocks and Shares JISA could be considered a gift to the child and therefore potentially subject to IHT depending on allowances and the death date of the contributor.

Beat inflation

Investing in a Stocks and Shares JISA inherently carries investment risk, meaning you may lose money, while paying into a Cash JISA doesn’t. While opening a Cash JISA might be the right option for some parents, it’s worth bearing in mind that the money you accumulate in one will be vulnerable to the effects of inflation, should prices increase at a higher rate than the rate of interest earned in the Cash JISA.

In 2025, the Investment Association said that £9,000 paid into a Cash JISA 18 years prior would have been worth £7,453 in real terms 18 years later, owing to the impact of inflation. In comparison, the same figure invested in a typical global equity fund via a Stocks and Shares JISA would have been worth £20,802.

Cash JISAs with interest rates that pay above inflation may exist, and it’s a good idea to consider both products. You can open both a Stocks and Shares JISA and a Cash JISA for your child, although the £9,000 annual allowance will be shared across both products. We do not offer Cash JISAs.

Things to consider before opening a Stocks and Shares JISA

Opening a Stocks and Shares JISA does require a parent to embrace a degree of investment risk and the possibility that the value of the investment could fluctuate over time, as with all investment products. There are a few other reasons that we acknowledge could make a parent pause for thought.

Lack of access

Nobody – child nor parent or guardian – can access the money that’s been paid into a Stocks and Shares JISA until the child in question reaches the age of 18. So if you haven’t already maximised your own ISA allowance, you might prefer to invest within your annual £20,000 limit and withdraw from your account when you want to pay for something on behalf of your child, or transfer money to them, subject to any tax that may potentially be payable. This approach would give you the benefits of a tax wrapper with more flexibility than a Stocks and Shares JISA. When withdrawing from your own ISA, tax benefits maybe lost depending on the terms of the ISA and if your ISA is not flexible, any tax allowances used in the year will remain used.

How will your child spend their JISA?

It is understandable that a parent or guardian may have concerns over how their 18-year-old will spend the money accumulated in a Stocks and Shares JISA – which could be worth a six-figure sum – given that the parent or guardian will have no say on how the money is used.

Almost 90% of parents surveyed by the Investment Association were confident that their children would use the proceeds of their JISA for its intended purpose. But it’s worth considering how you’re going to talk to your child about their JISA well in advance of revealing its total value when they can finally access their money.

J.P. Morgan Personal Investing wealth experts regularly support families as part of this process.

How to educate your child about their Stocks and Shares JISA

Giving children financial education can be challenging, and financial literacy levels among young people in the UK are low, compared to similarly advanced economies. Less than half of children and young people aged seven to 17 receive a meaningful financial education at home or at school, according to The Children and Young People’s Financial Wellbeing Survey conducted by the Money & Pensions Service in 2022. Over one in five people aged 14 to 17 feel anxious when thinking about money, the survey found.

It’s a good idea to give children the foundations of financial literacy before introducing them to investing. Younger children can grasp the concepts of earning, spending and budgeting. Then, when they reach their teenage years and start thinking about adulthood, slowly introducing your children to some investment principles, such as having a goal and starting early, can provide a good footing for them to begin their own investment journey.

The Stocks and Shares JISA can, in fact, be an excellent tool for educating your children about investing. “It demonstrates the benefits of investing for the long term and resisting the lure of cash, with financial objectives in mind,” says Exley.

“Setting investment goals with your children and discussing how they can use their money can hopefully increase the likelihood of them spending their wealth as you’d like them to, or at least mitigate against the risk of them spending it too quickly.”

Speak to our wealth experts

Our wealth experts can help you explore how you could invest more tax-efficiently while making the most of your annual allowances.

Our experts can offer conversations with families to discuss the pros and cons of using a JISA, forecast how much money you’ll need to contribute to meet any targets you might have, and how your child can best manage their newfound wealth once they reach the age of 18. They can provide support on how to use a JISA and how to manage the transition from JISA to ISA.

We can work with you to explore your options, answer questions and discuss how you could use a combination of investment products to accumulate wealth for your children. You can book a call to speak to one of our experts for free.

If you would like a personalised financial plan, we also have paid financial advice where we will review your finances and goals to help you build a financial plan with our recommended approach for you.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. This is general information, not personalised tax advice. ISA rules apply. To open our JISA, the child must be under 16 and funds can't be withdrawn until they turn 18. Tax rules vary by individual status and may change. Past performance and forecasts are not a reliable indicator of future performance. We provide 'restricted advice', meaning we only make investment recommendations on the products and services that we offer.