Investment outlook: summer check-in

Investment team

14 min

In this video update, key members of our investment team sit down with our host to reflect on the year so far and set out whether the themes they outlined in their annual outlook still hold true. The accompanying article provides additional detail as well as information on technical elements of the discussion.

At a glance:

- The first half of the year saw strong returns for investors despite the geopolitical turbulence. Global equities rose almost 10% and a traditional 60% equities / 40% bonds portfolio gained 7%.

- Two key developments stood out to us: 1) conflict in the Middle East lifted oil prices sharply, reviving concerns around higher inflation and the potential for higher interest rates, and 2) artificial intelligence-linked corporate earnings momentum stayed supportive.

- The big themes from our annual investment outlook from the start of the year are still largely intact, with some nuance. Key themes include the investment case for US equities still being compelling and the outlook for emerging market equities being positive.

- Key risks we continue to monitor include: whether AI-related capital expenditure could materially slow down; the potential for oil-driven inflation shocks; and weak fiscal discipline, with the UK a focal point.

Introduction

Welcome to our summer check-in on our investment outlook. We’re now through six months of the year, which is a good time to reflect on how 2026 has played out so far.

Our investment team analyses and evaluates the financial markets on an ongoing, daily basis, but the mid-year point offers an opportunity to reflect and assess long-term views.

Reflections on the year so far

Overview

Start-of-year expectation: “As we enter 2026, we remain largely positive about the potential for higher risk assets, such as equities, to deliver another positive year...Our optimistic outlook is based on several key beliefs, but above all, earnings growth – particularly in the US – remains supportive in our minds and is typically a necessary condition for equity markets to advance.”

The headline is that so far this year, global equities are up almost 10% to the end of June, and a typical portfolio with a traditional 60% equities and 40% bonds allocation split is up 7%.

As is normal in investing, these gains have not been linear, with March seeing a stumble in asset prices across many indices as conflict in the Middle East reared its head. However, this equity market sell-off was relatively short-lived, as both April and May saw notable recoveries and multiple new record highs for indices such as the S&P 500, which reflects the performance of 500 of the largest listed companies in the US.

Key market influences

To us, the first half of the year has centred around two main drivers:

1. Geopolitics putting inflation back in the mix

The start of the US-Iran conflict in late February and early March disrupted the oil market, pushing global energy prices higher. Inflation, which had been fading, rose back up the list of investors’ concerns. Energy costs are a key input for businesses and consumers. The sharp spike in oil prices raised concerns that this could feed through to higher prices for goods and services, which could in turn act as a brake on economic growth.

The pre-war consensus view had been that central banks may gradually continue their ‘easing’ efforts this year, where rates would fall slowly. That changed abruptly as investors weighed up how long the energy market might be disrupted by the closure of the Strait of Hormuz, a key trade route for the oil market. Markets began to price in potential interest rate rises by major central banks. By the end of June, this had started to settle somewhat as the geopolitical situation became slightly calmer. However, early July has seen further disruption in the region, which could alter the picture further.

Developments in the Middle East have mattered for equity markets, and even more so for bond investors. This is down to the potential inflation and interest rate implications, both of which are central for bond yields – the annualised rate of return paid by a bond to an investor. As the conflict progressed, we saw sharp swings in bond yields. Bond yields and prices have an inverse relationship, so when yields rise, prices fall.

We will continue to monitor the situation closely, especially how consumers react if we do see prices start to shift materially higher.

2. Earnings, earnings, earnings: with artificial intelligence driving the bus

Despite the conflict, in April investors began to re-focus on the US corporate earnings season, where large corporates release their financial results.

Earnings for the first quarter of the year were strong, especially in the US, but also in parts of emerging markets. A lot of that momentum is tied to spending to support activities of companies in the artificial intelligence (AI) space, which has moved from strength to strength of late.

The semiconductor industry, which includes producers of the physical chips that enable AI models, have been a huge driver of market returns recently. But as these market-leading companies have grown, their success and subsequent scale also bring concentration risk for investors.

When an index’s returns are being driven by a small number of companies, if the leaders wobble, the whole market can feel it, leading to heightened volatility. This has been visible in emerging markets, and we delve into this in more detail in theme two. We believe there are big opportunities in this space. It could, however, come with increased price movement for emerging market equity indices when there are economic or financial data releases, given the significant scale of these companies in the asset class.

Sticking to our convictions

It was difficult for investors to stay ‘pro-risk’ when the Iran war kicked off, given the potential implications for inflation. We saw other asset allocators reduce risk by trimming exposure to ‘risky’ assets such as equities amid the higher uncertainty, reflecting a ‘bearish’ shift.

In our view, that move was premature given the broader backdrop, particularly the strength of the US economy and an impressive corporate earnings cycle. The challenge was maintaining conviction through the highly volatile spring months, when investors could have been pulled toward short-term headlines. We stayed focused on the medium term and on one core question: how much did the situation add to recession risk, and could that derail markets?

Our conclusion was that recession risk would likely require a much more prolonged oil shock to rise meaningfully. The US economy still appeared to have a decent buffer, and the AI theme remained robust, despite the noise.

Reflecting on our 2026 outlook

We highlighted six key themes that we felt would shape the investment backdrop in 2026. We reflect on these themes below, analysing how they have played out, and how we think they will progress over the remainder of the year.

1) US equities continue to be compelling

Start-of-year expectation: “In 2026, we expect US equities to benefit from continued AI adoption, with the broader market likely to catch up as the advantages of AI spread and the overall strength of the US economy persists.”

Mid-year view: Theme intact

This theme certainly remains intact. We’ve seen the US economy show resilience despite the spike in energy prices, which is encouraging. Some of it is due to the surge in capital expenditure (CapEx) related to AI. CapEx involves businesses investing in long-term assets to support future operations and growth. In the context of AI, this covers spending in areas such as data centres, hardware and supporting infrastructure.

In the last quarter of 2025, AI-related CapEx increased by around +40% on an annualised basis, which increased further to +50% in Q1 2026. This is now spreading into other areas of the US economy. US gross domestic product (GDP) growth for the first quarter was 2.1% when annualised – extrapolated out to an annual figure to make comparison easier. Of this, AI Capex accounted for around one third (0.77%), a substantial chunk of growth for the US economy. For a deep dive on this topic, you can explore this article from our colleagues at J.P. Morgan Asset Management.

Looking at US equities year-to-date, returns have been around 10% to the end of June. However, the tech-focused Nasdaq rose 20%*, making the technology sector an outperformer vs. the broader US stock market.

Overall, we have seen a move away from the ‘Magnificent 7’, which includes companies such as Apple, Microsoft and Amazon. These can also be classified as the ‘AI spenders’, commonly also referred to as the ‘hyperscalers’. These are companies investing heavily in CapEx with the aim of benefiting from AI adoption via areas such as productivity gains and lower costs.

On the other side, we have the ‘AI earners’. This includes companies in spaces such as semiconductors and memory that can directly monetise AI.

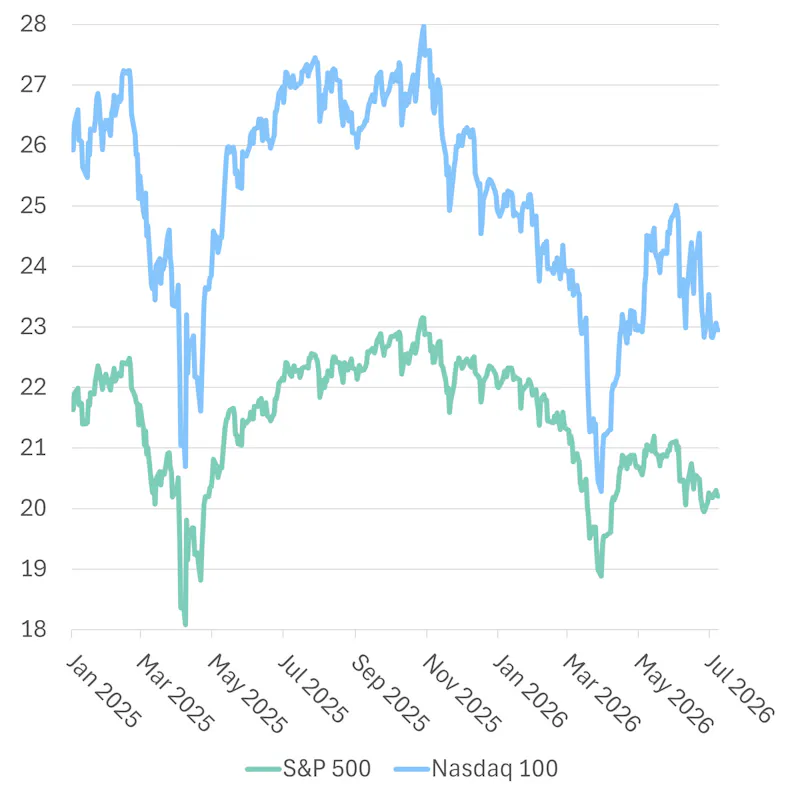

While there have been concerns around valuations, these have compressed as the market has ‘grown’ into its previous price-earnings ratio. This is a measure of a stock or index’s price relative to its expected earnings. The higher the P/E ratio, the more ‘expensive’ an asset could be viewed as, while the lower the ratio the more ‘value’ it may be deemed to have.

At the start of the year the Nasdaq was trading around 25 times 12-month forward earnings, while at the end of June this was closer to 23. The S&P 500 has moved from 22 to 20 over the same period.

12-month forward P/E ratios: US equities have started to ‘grow’ into their valuations on the back of a strong corporate earnings season

Source: Macrobond, J.P. Morgan Personal Investing. Data as at 8 July 2026.

2) The case for emerging markets (EM) is strengthening

Start-of-year expectation: “Our 2026 EM equity outlook is constructive but selective. A broad re-rating is possible if global conditions ease, but performance across different regions will likely continue to vary. Investors should focus on markets with credible reform stories, strong domestic demand and alignment with global structural themes.”

Mid-year view: Theme intact

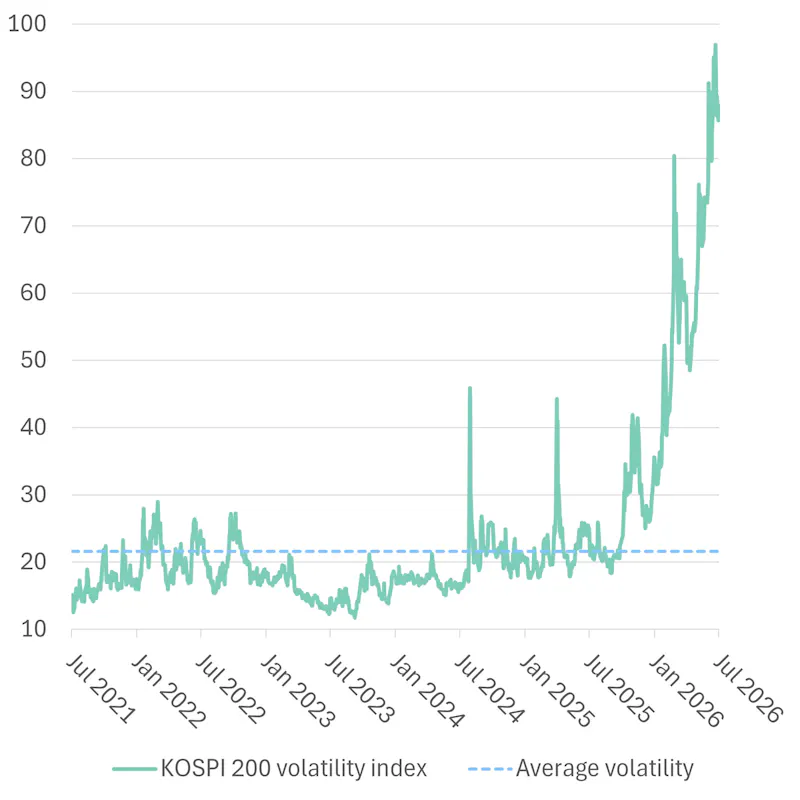

Emerging markets have been one of the best-performing regions year-to-date, up 24% over the first six months of the year. We have liked, and continue to like, parts of the region for their exposure to the ‘AI earners’ we just referenced, and these are principally based in South Korea and Taiwan.

We also entered the year constructive on the commodity story, supported both by the broader AI build-out and by infrastructure demand, which has favoured several Latin American markets.

China still faces meaningful economic headwinds, although beneath the surface the AI dynamic is also playing out, even if it is not front and centre yet.

Stock market performance in South Korea and Taiwan has been exceptional, but it has also brought bouts of extreme volatility, particularly in South Korea, where the market has at times traded more like a cryptocurrency (with a volatility of around 90 points vs. a historical norm closer to 20).

We remain believers in the fundamentals of the AI theme, but we are monitoring developments in Emerging Asia closely and will manage risk accordingly.

Higher volatility has accompanied higher returns in South Korea

Source: Macrobond, J.P. Morgan Personal Investing. Data as at 8 July 2026.

3) More ‘normal’ for bond markets in 2026

Start-of-year expectation: “Enjoying better yields in balanced portfolios – 2026 stands to be a year where bond yields make a positive contribution to portfolio income.”

Mid-year view: Theme intact

It has been a balancing act so far. In the brief risk-off episodes this year, bonds have largely fulfilled their traditional defensive role and provided income within portfolios. However, as mentioned earlier, events in the Middle East have challenged the assumption of a smooth central bank easing path and have also raised questions around government spending plans.

We have also seen some developed market central banks pivot toward tighter policy in response, most notably with the European Central Bank (ECB) hiking by 25 basis points.

Since the Memorandum of Understanding between the US and Iran agreed in June, which set out steps for mutual de-escalation, bond yields have fallen. This reflects a compression in the inflation premium embedded in bonds.

At time of writing, the Bank of England (BoE) is not expected to ‘tighten’ (which can include increasing interest rates) this year, despite the potential for energy costs to push up prices.

Overall, we remain circumspect on government debt, preferring credit exposure, while noting that government bonds do look attractive on valuation grounds.

US and UK 10-year bond yields fell in June but remain heightened by historic standards

Source: Macrobond, J.P. Morgan Personal Investing. Data as at 7 July 2026.

4) Don’t underestimate the influence of commodities

Start-of-year expectation: “In a dynamic world where the energy mix of consumption and demand continues to evolve and energy efficiency is being improved, oil remains an important part of our lives.”

Mid-year view: Theme intact, but with nuance

Oil was expected to see price compression as the year progressed, particularly in the first half, on the view that a supply glut would gradually normalise into the second half. Instead, we’ve seen the opposite, with prices spiking as a result of the conflict in the Middle East.

What’s notable, at least in the US, is that the impact of the spike has remained largely confined to transportation. That may reflect businesses choosing to look through the oil shock on the assumption of a quick resolution.

As we look towards the second half of the year, prices sit between $70 and $80 dollars per barrel, down sharply over June. Between March and May, Brent crude oil – the global oil price benchmark – bounced between $90 and $110, up from about $60 at the start of the year. Given this drop-off, there is scope for the inflationary impulse from geopolitical events to remain contained.

5) Fiscal discipline found wanting

Start-of-year expectation: “Little cushioning for fiscal spending - a lack of discipline and political will across the west is no longer cushioned by ultra-low interest rates or central bank support.”

Mid-year view: Theme intact

This theme centres around the need for governments to appropriately balance budgets and not rely so heavily on the debt markets to fund future spending. As investors, this is something we remain on high alert for. Governments around the world are increasingly caught between voters’ demand for higher spending and bond markets that closely scrutinise fiscal plans and budget credibility.

In the near term, there does not appear to be any great urgency to correct these imbalances, but they remain a looming risk. Some countries will feel the pressure more acutely than others. Governments around the world will have to tread a narrow path between spending, investment, and growth. Meanwhile, the repercussions of failing to address the underlying fiscal challenge continue to compound over time.

We are monitoring the UK closely, particularly given the political situation and the planned change of leadership by the governing Labour Party.

6) Risks in an expensive market

Start-of-year expectation: “Key risks worth highlighting include: if the US Federal Reserve becomes significantly less supportive in its rate-cutting cycle, lower-than-expected GDP growth, US technological stocks reversing their AI optimism, and a genuine fear of the US entering a recession.”

Mid-year view: Theme intact, but with nuance

To date, the clearest beneficiaries have been AI infrastructure within IT: chips, memory, and the data centre supply chain, as well as energy and power-linked buildouts, all driven by surging demand for hardware.

A key point to watch is around the level of AI optimism across parts of the US technology sector, particularly any developments that could slow the AI CapEx that we outlined earlier. At this stage, however, some signals look less like a true reversal and more like a shift toward tighter cost governance and optimisation.

As AI costs increasingly flow through to end users and individual business units, some large firms are beginning to actively manage token usage. Rather than indicating demand destruction, this may simply reflect a transition from broad-based experimentation to more disciplined scaling, with workloads migrating toward cheaper and more efficient models.

That kind of substitution can reduce unit costs and, over time, expand the universe of return on investment-positive use cases. In turn, aggregate demand, and upstream infrastructure spending, can remain supported, even as the composition of growth shifts.

For markets, earnings periods will continue to be watched closely by investors. Anything that threatens the ongoing delivery of earnings growth, or changes the outlook for future earnings growth, could have meaningful ramifications for equity markets.

We believe the investment backdrop remains constructive

We believe that the backdrop remains supportive for financial markets in the second half of 2026. As we saw in the first half of the year, surprises can materialise, but markets are typically good at refocusing on the fundamentals.

As always with investing, there is the possibility of volatility in any period. But it is a feature of being in the markets. It is our view that staying invested, even during periods of volatility or negative news flow, remains the best strategy for generating attractive long-term returns. This is something that was emphasised in April and May as markets recovered strongly from March’s sell-off.

About this update: All figures in the article, unless otherwise stated, are to the end of June 2026. Data in the video is to 26 June 2026.

Sources: MacroBond, J.P. Morgan Personal Investing and Bloomberg.

*In the video, we state that the Nasdaq was up 17%. This was to 29 June.

Risk warning

As with all investing, your capital is at risk. The value of your portfolio can go down or up and you may get back less than you invest. Past performance and forecasts are not reliable indicators of future performance. We do not provide investment advice in this article. Always do your own research.